The U.S. economy faces a widening gap: rising inflation on one side and a lack of employment on the other. According to mainstream Keynesian theory, this situation shouldn't occur. This is because a slack labor market should lead to lower wage growth and consumer demand, and price inflation should subside. The experience of economies in the 1970s disproved this theory, which was supposedly supported by the so-called Phillips curve (the trade-off between rising prices and unemployment). Inflation erupted, and unemployment soared. The 2010s, following the Great Recession, disproved this theory again, when inflation in major economies fell back to near zero and unemployment reached historic lows. In the post-COVID-19 period from 2021 to 2024, inflation has risen sharply, but unemployment has remained low.

Why is Keynesian theory wrong? Because Keynesian theory assumes that aggregate demand drives spending and prices. If demand exceeds supply, prices will rise. However, in both periods, both the 1970s and the 2010s, the driving force was supply, not aggregate demand. In the 1970s, economic growth slowed due to a plunge in capital profitability and investment growth, and then oil producers restricted energy supply, causing crude oil prices to soar. In the 2010s, economic growth was slow and inflation fell, but unemployment did not rise. In the 2020s, the post-pandemic recession led to the collapse of global supply chains, rising energy prices, and a decrease in skilled workers. This was a supply-side problem. Monetarist theory also exposed itself during these times. Central banks—particularly the Federal Reserve under Ben Bernanke, a disciple of Milton Friedman, the founder of monetarism, who argued that inflation was essentially a monetary phenomenon (meaning that the money supply drove up prices)—believed that the answer to the Great Recession of 2008-2009 was to lower interest rates and increase the money supply through so-called quantitative easing (QE). This meant the Fed "printed" money and bought government and corporate bonds from banks, which in turn was expected to increase lending (the money supply) to businesses and households, boosting consumption. But this did not happen. The real economy remained depressed, and all the monetary injections merely inflated financial asset prices. Stock and bond prices soared. Once again, monetarism ignored the true driver of economic growth, spending, and investment: the profitability of capital, or the supply side. Last February, I wrote an article suggesting that the US economy was showing signs of "stagflation." Stagflation refers to a situation in which national output and employment stagnate or grow slowly, while price inflation continues to rise or even accelerates. The US economy has clearly been slowing. Quarterly growth rates have been volatile, primarily due to large fluctuations in imports. Imports surged early this year as businesses sought to get ahead of Trump's import tariffs. Then, as the tariffs began to affect imported components needed by industry, real GDP growth slowed. But in the first half of this year, under Trump's administration, the economy slowed significantly. Indeed, economic growth is declining, approaching what some analysts call "stall speed"—the rate below which an economy enters a recession (with a direct decline in GDP). The US economy hasn't yet fallen into recession because corporate profits are still growing and a boom in artificial intelligence investment is driving growth in key economic sectors. But stagflation is no longer the shimmering speck in the economic air it was in early 2025.

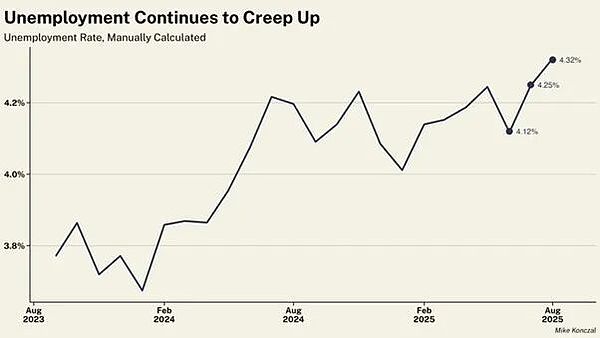

Take employment as an example. Job growth is slowing rapidly and the unemployment rate is also rising.

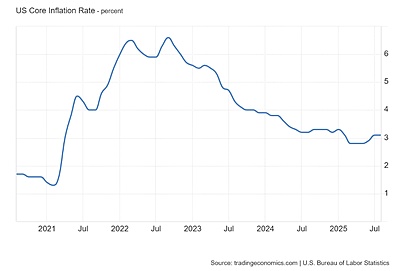

Net employment increased by only 22,000 jobs in August, while June's net employment was revised down to a decrease of 13,000 jobs. Trumponomics assumes that tariffs will increase manufacturing jobs while federal layoffs will free up more workers. This simply isn't happening. Manufacturing jobs are being lost almost as fast as the federal workforce (-12,000 vs. -15,000). Job growth is slowing across nearly every industry. Unemployment has been particularly severe among men. Over the past four months, 56,000 men have lost their jobs. This is largely due to a sharp decline in the labor force caused by Trump's crackdown on immigration policies. While U.S. Immigration and Customs Enforcement (ICE) is conducting mass arrests and deportations, the number of foreign-born workers in the United States has begun to shrink after years of rapid growth. Native-born workers have not benefited, with their unemployment rate reaching its highest level since the end of the pandemic. Trump fired the director of the Bureau of Labor Statistics after it released very weak job growth data. But annual revisions to employment data since then have resulted in 911,000 fewer jobs added in the year ending March 2025. Firing the messenger doesn’t change the essence of the message. U.S. job growth has slowed to a level not seen outside a recession in more than 60 years. The slowdown in job growth isn’t due to weak demand but rather to supply growth drying up as immigration declines, manufacturing continues to decline, and a government agency and workforce have been gutted by Trump. The fundamental problem is that insufficient demand isn't holding back U.S. manufacturing; it's labor. The number of workers able and willing to work on factory floors is shrinking. According to the U.S. Bureau of Labor Statistics, there are currently nearly 400,000 unfilled manufacturing jobs. A decrease in productive workers means slower economic growth. The Federal Reserve is helpless in this situation, whether by cutting interest rates or increasing monetary injections (quantitative easing). Even if Trump succeeds, fires some Fed governors, takes control of the Fed, and slashes its policy rate, it will only further fuel speculative frenzy in the stock market and do little to improve the productive sectors of the economy. The current Fed board is reluctant to cut rates because they fear accelerating inflation. Inflation is already rising. The latest Consumer Price Index (CPI) accelerated to 2.9% year-on-year in August 2025, well above the Fed's 2% inflation target. The Fed prefers to track what it calls personal consumption expenditures (PCE) inflation. This rate consistently falls well below the average price increase for consumer goods consumed by US households. But even PCE inflation remains above the Fed's 2.6% year-on-year target. Core inflation (excluding energy and food prices) remains stubbornly stuck at 3.1% year-on-year.

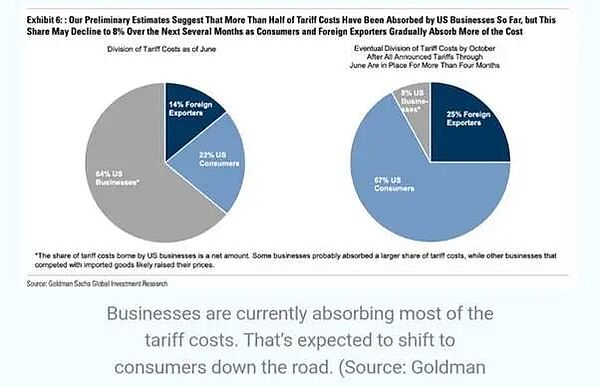

Again, the rise in inflation is not due to demand for goods and services outstripping supply; but rather to slower production and higher production costs, especially in services such as utilities and health insurance. Trump administration officials argue that tariffs have no impact on inflation. But if that were true, it would mean a "supply shock" in prices would have occurred regardless. Admittedly, the impact of tariffs has been limited so far. That's because as soon as Trump started throwing a tariff tantrum, U.S. importers rushed to stockpile inventory to get ahead of any tariff increases. This is why U.S. imports soared in the first half of 2025 and the U.S. trade deficit worsened sharply. In addition, some exporters to the United States have lowered prices to absorb the impact of tariffs on import prices. But tariff increases will eventually be reflected in consumer prices. An analysis by Goldman Sachs shows that about 22% of tariff costs have been passed on to consumers. Goldman Sachs estimates that this proportion will eventually rise to 67%.

Given that effective tariffs on imports are currently around 18% (up from around 4% before Trump took office), and that imports account for around 14% of US GDP, this can only mean that inflation willrise further

Over the next few years of a Trump administration, corporate and income tax cuts for high earners will reduce potential revenue by far more than the increase from higher tariffs. In fact, these tax cuts will constitute the largest transfer of income from poor to rich through a single government law in history. Tariff revenue will not reduce the federal government’s annual deficit, which currently stands at over 5.5% of GDP (even if growth slows slightly). In fact, the annual deficit is projected to rise to 5.9% of GDP over the next decade, and the public debt-to-GDP ratio is projected to reach 125% of GDP. Rising public debt ratios are another concern for government bond investors, pushing up bond yields no matter how much the Fed lowers short-term interest rates.

American families are feeling the economic pressure. Consumer confidence in the economy has plummeted to one of the lowest levels this century, on par with levels during the financial crisis and the 1980s recession.

The weakest parts of the business community are struggling. 446 companies have gone bankrupt so far this year, a 15-year high. I pointed out at the beginning of this article that the U.S. economy is entering a period of "stagflation," a period of rising inflation and unemployment. Stagflation shows that both Keynesian and monetarist theories of inflation are wrong. This means that no matter what the Federal Reserve does with interest rates or money injections, it will have little effect on inflation or employment—the central bank's alleged goals. Whether inflation and unemployment fall depends on whether U.S. real GDP and productivity growth recover. That, in turn, depends on whether business investment continues to rise. Ultimately, it depends on whether corporate profitability and profits remain unchanged or decline. So far, they haven't, but downward signs are emerging.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Kikyo

Kikyo