Of the current approximately $27 billion in RWA AUM, about $2.7 billion has entered the lending market and is being used as collateral, yield strategies, or revolving leverage. The assets truly being adopted by DeFi are not the largest government bonds, but rather credit assets with more positive yield spreads, especially categories like Maple, Aave, Morpho, Kamino, and reinsurance. The open permissions, easy integration, and cross-chain distribution design are becoming the core engine for the spread of RWA.

The Rise of Composable RWA

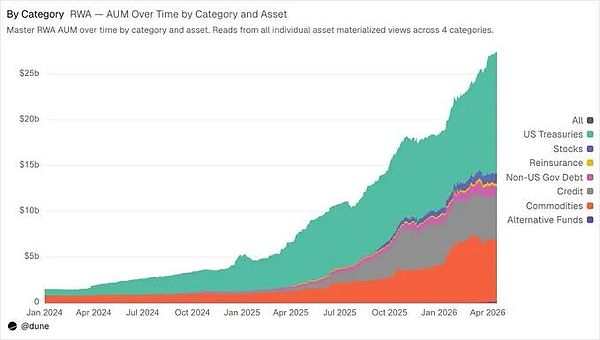

$27 billion in tokenized RWA, but only about $2.7 billion has actually been deposited into the decentralized lending market—as collateral, injected into treasuries, or used for yield strategies. It has grown rapidly from almost zero in just one year.

This article will explore where this capital is flowing, what is driving it, and what it foreshadows. Background: From Regulatory Clarity to Composable Capital Three regulatory milestones in late 2025 and early 2026 accelerated the tokenization process. In July 2025, the GENIUS Act established the first comprehensive framework in the U.S. for payment-based stablecoins, requiring 1:1 reserve backing and clear regulation. In March 2026, the SEC and CFTC jointly classified major blockchain tokens as digital goods, not securities. A few days later, the SEC approved Nasdaq to trade and settle tokenized stocks and ETFs on its main market. These milestones fueled an already accelerating trend. Stablecoins—the settlement layer for tokenized assets—saw their total supply surpass $330 billion, a 12-fold increase since 2020. During the same period, the number of active stablecoins grew from 31 to 215. Tokenized RWA followed a similar trajectory, with AUM growing 27-fold in two years to approximately $27 billion, expanding from a few categories to the seven categories we track in the Overview Dashboard, including reinsurance and stocks. Beyond the surface-level AUM figures, a more crucial question is: how much of this capital is actually playing a role within DeFi? Approximately $2.7 billion worth of RWA tokens have been actively deposited into various DeFi lending markets—representing about 10% of the $27 billion in tokenized AUM. This 10% was virtually non-existent a year ago. Composability—the ability of a tokenized asset to be used as collateral, lent out, and circulated across different protocols and on-chain yield strategies—is arguably the most promising advantage of tokenization.

Source:dune.com/queries/6972565/?utm_source=share&utm_medium=copy&utm_campaign=query Note: Our statistics are based on RWA tokens deposited or provided to lending protocols—only collateral and vault supply are included. We exclude borrowed amounts and stablecoins provided as lending liquidity to focus on RWA assets actually used in DeFi operations. All data is as of April 16, 2026.

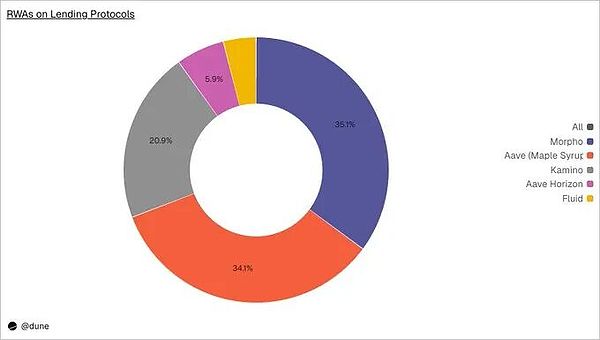

($957 million) — 41 RWA assets listed on 10 chains without permission.

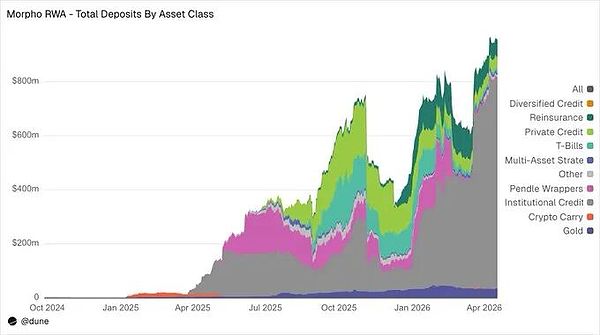

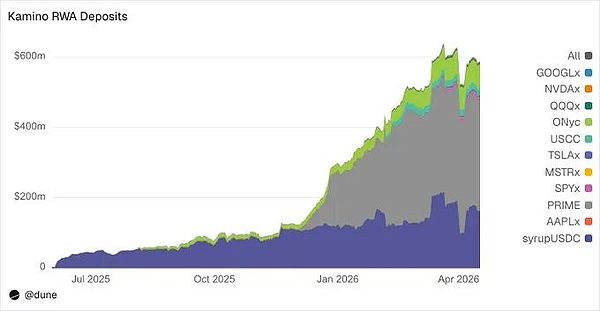

Specialized curators like Gauntlet and Steakhouse manage the vaults, allocating capital to these markets and building structured leverage strategies on top of tokenized real-world assets. @aave (broader market) ($929 million) – Maple's syrup tokens are distributed across Plasma, Base, and Ethereum. Institutional credit flows permissionlessly to where lending economics are optimal. @kamino ($587 million) – The largest lending protocol and RWA platform on Solana. PRIME $315 million (HELOC lending revenue), syrupUSDC $161 million, ONyc $71 million (reinsurance), USCC $18 million, plus the xStocks market (seven tokenized stocks totaling $21 million).

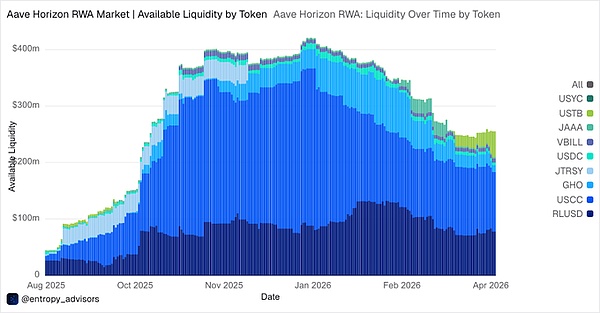

Aave Horizon ($161 million) – An institutional, permissioned RWA marketplace on Aave.

Tokenized assets are not necessarily used

There is a significant divergence between the assets that dominate tokenized AUM and the assets that are actually deposited as collateral in lending protocols. The two rankings are almost reversed.

Source:dune.com/queries/7327377/?utm_source=share&utm_medium=copy&utm_campaign=query US Treasury bonds account for 48.5% of tokenized AUM ($13.2 billion), but only 2% of DeFi deposits. Credit assets account for 17% of AUM, but about 80% of deposits. Commodities account for 25.2% of AUM, but only about 1%. The dominance of credit assets stems from the simple fact that it makes sense. @maplefinance's syrupUSDC yields approximately 6%, while T-Bills offer around 3.5%. This creates a positive carry trade when your collateral earns 6% and you can borrow stablecoins at 3%. Curators like @gauntlet_xyz build on this with explicit circular strategies: collateralize RWA, borrow, and buy more. This is a designed, risk-controlled leverage—which explains why credit assets are present on all major lending platforms: $957 million on Morpho, $929 million on Aave, and $476 million on Kamino.

Source:dune.com/queries/6912382/?utm_source=share&utm_medium=copy&utm_campaign=query In addition to existing categories, reinsurance is becoming a truly new class of combinable assets.

Source:dune.com/queries/7332182/059a5dd3-7eae-4519-8504-35f3e9f32038?utm_source=share&utm_medium=copy&utm_campaign=query Tokenized stocks are also entering DeFi: SPYx (US$7.9 million on Morpho),

The collateral portfolio is changing in real time

The dominance of high-yield credit assets may partly be a matter of timing. Aave Horizon provides the clearest evidence of this.

When Horizon launches in August 2025, USCC—@SuperstateInc's Crypto Carry Fund—provides approximately 15% of the APY through its basis trading on crypto futures. This yield makes it account for 93% of all RWA collateral.

Although T-Bill products were launched, they received almost no interest. Subsequently, as basis spreads narrowed, USCC yields compressed to approximately 4%, gradually converging with T-Bill yields of 3% to 4%. As a result, USCC's collateral share decreased from 93% to approximately 67%, while USTB surged from less than $1 million to $45.6 million in 30 days—a 570% increase. As the yield gap narrowed, the market is diversifying.

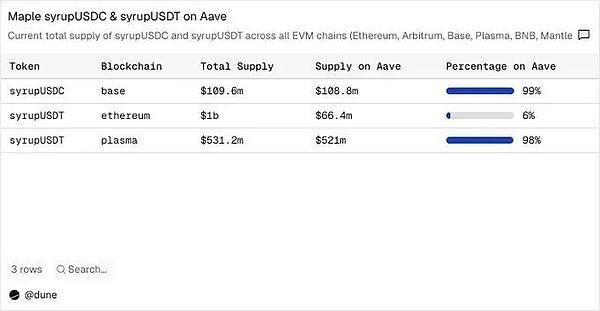

Source:https://dune.com/entropy_advisors/aave-horizon-rwa This is not only important for Horizon. If credit yields continue to compress across the market—which often happens in mature markets—then the collateral portfolios of all platforms are likely to become more diversified. The assets that dominated the first wave (high-yield credit) may not continue to dominate the next wave. Factors such as risk characteristics, regulatory acceptance, and settlement mechanisms will begin to become more important. @pendle_fi adds another dimension to this evolution. Its principal tokens (PTs)—tokens that allow users to lock in fixed returns on RWA products—account for $58 million in Morpho deposits. Pendle also provides direct RWA marketplaces for thBILL and mTBILL, incorporating yield curve trading into the composability stack. As more RWA products launch on Pendle, fixed-rate strategies will become another channel for RWA distribution. Maple Syrup is the clearest example. SyrupUSDC and syrupUSDT are permissionless ERC-20 tokens—technically, they fall somewhere between stablecoins and RWAs because they are pegged 1:1 to USDC/USDT, but their yields come from institutional credit. We categorize them as RWAs because their underlying exposure is real-world lending. Anyone can mint, trade, or deposit them into any lending protocol. No KYC, no whitelisting, no partnerships required. The result is that 98% of syrupUSDT on @Plasma and 99% of syrupUSDC on @base are actively deployed to Aave. Morpho curators like Gauntlet independently built leveraged treasuries without needing to coordinate with Maple. syrupUSDC also reached $161 million on Kamino (Solana).

Source:dune.com/queries/7324965/?utm_source=share&utm_medium=copy&utm_campaign=query Each new integration increases utility; utility attracts capital, and capital, in turn, justifies further integration. It is this flywheel effect that naturally distributes the $929 million across the three chains. This is important because distribution is widely recognized as the number one challenge in the industry. @centrifuge's Tokenization Outlook 2026 report shows that 86% of operators believe that expanding distribution for existing products is more important than launching new ones. Maple's case study on Aave demonstrates that permissionless composability itself is a distribution channel.

Frontline: $1.85 billion has been tokenized, $13 million is composable

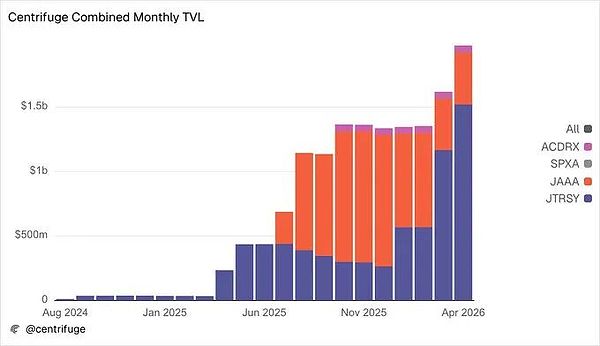

Centrifuge demonstrates the opportunities and gaps in RWA.

Centrifuge demonstrates the opportunities and gaps in RWA.

Centrifuge demonstrates the opportunities and gaps in RWA.

It is one of the largest tokenization platforms, with its institutional product AUM approaching $2 billion: JTRSY (a tokenized US Treasury bond fund) at $1.52 billion, JAAA (a tokenized AAA-rated CLO fund) at $403 million, ACRDX (Apollo's diversified credit fund) at $52 million, and NEDUNO's SPXA (the first tokenized S&P 500 index fund) at $3.7 million. However, only about $13 million of this is composable in DeFi.

Source:dune.com/queries/5534552/?utm_source=share&utm_medium=copy&utm_campaign=query This gap is attributed to timing and design. The deRWA wrapper is license-free, but it won't be available until September 2025. On the other hand, the licensing design of other mature products slows down the integration pace. Liquidity remains thin. But integration is accelerating. Resolv has committed $100 million in JAAA deployments on Horizon. Falcon Finance is using JAAA and JTRSY as collateral for USDf. Grove is deploying $250 million on Avalanche. LayerZero supports distribution across 165+ networks. And deSPXA—a DeFi wrapper around Centrifuge’s S&P 500 fund—has reached $3.6 million in TVL and $7.9 million in DEX trading volume, demonstrating early organic activity and the potential of the deRWA path: a permissionless wrapper operating alongside a permissioned product aimed at institutions.

Three Conclusions

Growth rate is more important than current size. There are $2.7 billion in RWA deposits in the DeFi lending market—about 10% of the $27 billion in tokenized AUM. But this $2.7 billion was almost non-existent a year ago. The absolute number is still small, but the growth rate is more important.

Being tokenized is not the same as being used. US Treasury bonds account for 48.5% of tokenized AUM, but only 2% of DeFi deposits.

What is tokenized is not necessarily used.

Credit assets account for 17% of AUM but 80% of deposits. Higher yields create positive carry trades, sufficient to support a leveraged cycle—credit yields above 6% are feasible, while 3.5% government bond yields are not. However, as the macroeconomic environment changes and yield spreads between different asset classes shift, the collateral composition will adjust accordingly, with new assets and emerging categories (such as reinsurance) constantly emerging. Permissionless access has driven distribution. Maple's syrup token—a hybrid between RWA and stablecoins—has exceeded $1 billion in market capitalization across four chains: Aave and Kamino. This token was designed for composability from the outset, so the market has naturally combined it. Easily accessible assets are adopted faster. Assets requiring whitelisting are catching up, but at a slower pace. All data cited in this article is available for free on Dune. You can start with the RWA Overview categorized by AUM, or delve into the dashboards for each platform: Morpho RWA, Aave Horizon, Maple on Aave, Centrifuge, and Kamino RWA TVL. Data as of April 16, 2026.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Anais

Anais