False Alarm: Cointelegraph's Blunder About iShares Bitcoin Spot ETF Pumped Bitcoin Price to 30K

Cointelegraph tweeted that SEC approved iShares' Bitcoin (BTC) Spot ETF, but was confirmed to be false by BlackRock.

Aaron

Aaron

Author: Lisk; Translator: Eric, Foresight News

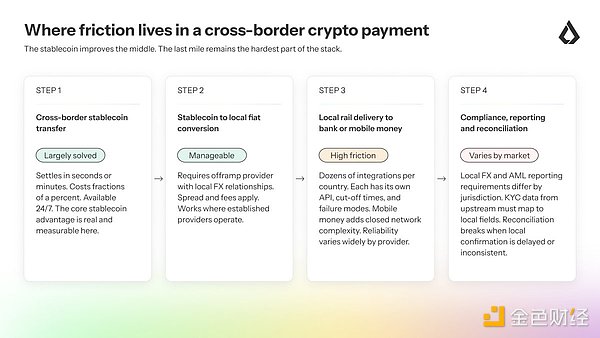

Stablecoin channels have indeed significantly improved the cross-border aspect of international payments. However, the part that remains consistently problematic is the final delivery of funds to local accounts and wallets.

The value of stablecoins in cross-border payments is widely recognized and largely validated at the wholesale level. Transferring value from one country to another using USDC or USDT is faster than traditional proxy banking chains, cheaper than most traditional wire transfers, and available 24/7. For the "middle segment" of cross-border payments—the part that crosses borders—stablecoins represent a real infrastructure advancement.

The unresolved issue is the last mile. Reliably and massively converting settled stablecoin balances to local fiat currency in accordance with local regulatory requirements and sending them to the correct bank accounts or mobile money wallets—this is where most of the friction, costs, and failures in cross-border crypto payments are truly concentrated.

Stablecoin channels shorten the distance between countries, but the "last mile"—the distance between stablecoins and those who truly need the money—remains the most difficult part to build in the entire technology stack. What exactly is the "last mile"? The last mile of cross-border crypto payments involves four steps, the first three of which are largely solved. Stablecoin transfers reach the service provider's wallet after cross-border settlement—this step is quick and inexpensive. The provider needs to convert these stablecoins into local fiat currency, usually through local forex partners or internal reserves—this step has costs and spreads, but is operationally manageable in most channels. Then the fiat currency needs to be sent to a local payment channel: Real-time Gross Settlement (RTGS), Automated Clearing House (ACH), Instant Payments Network, or mobile money platform—this is where reliability issues begin to surface. Finally, payments need to be reconciled, reported, and considered regulated cross-border or foreign exchange inflows in many jurisdictions—this step adds compliance overhead, and varies greatly across different markets. Friction doesn't accumulate evenly across these steps. Where offshore exchange providers have established stable relationships with local banks and forex partners, conversion and liquidity are manageable. It's the integration of local payment channels that reveals reliability problems: each country has multiple banks, multiple mobile money operators, different technical APIs, different deadlines, and different error handling mechanisms. A provider serving ten markets needs to maintain and monitor dozens of independent integrations, each of which can fail independently. Compliance and data requirements add another layer of complexity: KYC (Know Your Customer) and KYB (Know Your Business) data collected upstream in the payment chain must be translated into local reporting fields, thresholds, and documentation requirements, which vary across different jurisdictions. Reconciliation—matching stablecoin settlement records with local disbursements (payment) confirmations—is theoretically simple, but very difficult in practice, especially when local payment confirmations are delayed or arrive in incompatible formats. Stablecoins solve the "distance" problem; the last mile solves the "delivery" problem. These are two different problems requiring different infrastructures.

The last mile relies on local outbound providers—companies that convert stablecoins into local fiat currency and send them to local banks and mobile money channels. In most emerging markets, this sector is highly fragmented, of varying quality, and vulnerable to shocks.

In Africa, Yellow Card has built a pan-African stablecoin channel covering more than twenty markets, integrating banking and mobile money infrastructure, and positioning itself as an offshore exchange provider for global platforms such as Coinbase, Block, and PayPal.

Kotani Pay takes a complementary approach: providing a blockchain-to-mobile payments API for East and West African markets, using USSD instead of an internet connection, allowing even feature phone users to receive stablecoin-backed payments without a smartphone or bank account. These are meaningful infrastructures, but they are not all-encompassing—coverage gaps remain in specific countries, specific banks, and specific mobile money operators. In Latin America, Bitso's unified payments architecture executes the receiving and sending functions of the region's major local payment channels (including Pix in Brazil, SPEI and ACH in Mexico) through a single API, with foreign exchange and stablecoin settlement embedded at the underlying layer. This architecture is effective because Bitso has invested heavily in addressing the most challenging aspects: building and maintaining local channel integrations, foreign exchange relationships, and compliance infrastructure in each operating market. Building similar capabilities from scratch takes years, not months. Besides major providers, there are numerous smaller withdrawal operators serving specific channels, varying significantly in uptime, liquidity depth, compliance capabilities, and operating terms. When smaller offshore exchange providers experience disruptions—whether due to regulatory uncertainty, liquidity crises, or changes in banking relationships—payments queue, reconciliation backlogs increase, and operators are forced to manually route to secondary providers with different formats, KYC standards, and fees. This risk is not theoretical but an operational reality when relying on unreliable, non-standardized infrastructure. Cost data clearly shows the contribution of the last mile to total payment costs. World Bank remittance data for Q1 2025 shows the global average remittance cost was 6.49%. In sub-Saharan Africa, costs are higher—averaging around 8% at the beginning of 2025. The cost of stablecoin transfers themselves may be well below 1%. However, when foreign exchange conversion, local payment fees, mobile money charges, and compliance expenses are added, the end-to-end cost of many African channels rises back to the 7% to 8% range. The savings from stablecoin channels are real, but a large portion is offset by the last mile. Mobile Payments and the Last Mile: For hundreds of millions of people in parts of Africa and Asia, mobile payments are not just an option, but the primary financial account. The GSMA's 2026 State of the Industry report shows that there are 2.3 billion registered mobile payment accounts globally, with 593 million monthly active users in 2025, and transactions processed through mobile money wallets exceeding $2 trillion—doubling in just four years. The majority of these active accounts are located in sub-Saharan Africa, where mobile payment accounts are often the only physical financial account available to a large portion of the population. For businesses making cross-border stablecoin payments in these markets, reaching the recipient typically means reaching their mobile money wallet, not their bank account. This creates a series of specific technical and regulatory challenges on top of the fragmented withdrawal problem. Mobile payment networks are closed systems. M-Pesa, MTN MoMo, Airtel Money, OPay, and Wave each have their own integration models, technical APIs, compliance rules, and operational characteristics. A provider looking to deliver to mobile money wallets in five African countries needs to manage fifteen to twenty separate integrations, each requiring direct business relationships with mobile network operators, ongoing technical maintenance, and real-time monitoring. When M-Pesa in Kenya experiences a failure, all payments through that channel are affected until service is restored. By this time, the provider's stablecoin settlement may have already been successfully completed; the only thing stuck is the final delivery step the recipient is waiting for. Regulatory aspects further add complexity. Mobile payment transactions exceeding prescribed thresholds require KYC verification at the wallet level. In many jurisdictions, cross-border mobile money flows are considered foreign exchange inflows and trigger reporting requirements. In some markets, the regulatory boundaries for stablecoin-to-mobile payment delivery are still being defined, leading to uncertainty about what compliance documentation is required and who is responsible. Kotani Pay's direct integration with mobile money operators via USSD (allowing payments without internet or a bank account) demonstrates that innovative infrastructure can reach previously excluded populations; while Chipper Cash's partnership with Stable in December 2025 to build stablecoin payment channels in Africa illustrates that even established players continue to invest in solving the last-mile problem, rather than treating it as a completed task. What does reliable last-mile infrastructure require? Companies capable of reliably enabling stablecoin cross-border payments at scale share a series of common characteristics that distinguish them from smaller, less efficient providers unable to meet the needs of businesses. **Single Integration, Multiple Channels:** The operational overhead of maintaining dozens of independent integrations is a major reason why last-mile infrastructure is expensive and difficult to replicate. Abstracting this complexity to a provider behind a single API—offering only one integration point externally and resolving to multiple local channels internally—creates significant operational leverage for its clients. Thunes' expansion to support stablecoin payments from 11,500 banks via SWIFT connections, connecting over 500 million stablecoin wallets in 140 countries globally, is a global application of this principle: one connection point, corresponding to a vast network below. **Deep Local Licensing and Relationships:** Technical integration is necessary, but far from sufficient. Reliable last-mile delivery requires establishing business relationships with local banks and mobile payment operators, obtaining regulatory approvals in each market, and compliance systems that meet local anti-money laundering and foreign exchange requirements. These take years and significant capital to build. New entrants cannot quickly replicate this, which is why most reliable last-mile providers in the market are companies that invested in regulatory infrastructure before transaction volume arrived. Enterprise-level operations: The difference between a last-mile solution that works well for small transactions and one that works well for enterprise-level traffic lies primarily in operations, not technology. It requires multiple banking partners per channel for redundancy, real-time switching between different payment channels when one channel fails, real-time monitoring of payment status across all integrations, and a predictable Contractual Service Level Agreement (SLA). Manual processes handling a few hundred transactions per day will collapse when they reach tens of thousands per day. The reconciliation layer—the internal ledger that tracks every payment from stablecoin receipts and foreign exchange conversions to local inbound confirmation—must be automated and auditable to support large-scale operations. Last-mile is not a problem with a single technological solution. It is an operational and regulatory problem that requires continuous, market-to-market investment in infrastructure, relationships, and compliance. Why is this crucial for operators? For businesses conducting cross-border stablecoin payments, the last-mile problem is far from an abstract concept. It directly impacts which channels you can reliably serve, your actual end-to-end costs, and the customer experience when payments fail to arrive on time. The practical significance lies in this: channel selection is not merely a business decision about where there is demand, but a decision about where the infrastructure for reliable last-mile delivery exists. If a channel offers fast and cheap stablecoin settlement, but local offshore exchanges are highly fragmented, have limited capacity, or are subject to regulatory uncertainty, then the payment experience of that channel becomes unpredictable. Stablecoins fulfill their purpose, but the last mile fails. For businesses building payment products rather than simply using them, the last-mile problem is even more fundamental. Decisions about which local channels to integrate, which offshore partners to rely on, how to handle mobile money delivery, and how to manage compliance in the payment process are all product-level decisions that determine which markets you can serve and the quality of your service. Providers that have solved this problem—Yellow Card in Africa, Bitso in Latin America, and Thunes globally—have achieved this through years of sustained investment in these decisions. Stablecoin gateways are becoming a commodity, while last-mile infrastructure is far from it.

Cointelegraph tweeted that SEC approved iShares' Bitcoin (BTC) Spot ETF, but was confirmed to be false by BlackRock.

AaronSui under the investigative lens of the FSS with allegations centred on inaccurate reports pertaining to its circulating supply and the purported gains derived from staking activities.

Catherine

CatherineEtherHiding is a new technique employed by hackers to infiltrate websites powered by WordPress. Once in, they embed malicious code designed to pilfer partial payments from blockchain contracts.

Kikyo

KikyoFollowing the initial report on Monday, BC Technology's Share Price fell by 22 per cent.

Clement

ClementIn a startling development during the ongoing criminal trial of FTX founder Sam Bankman-Fried, a comprehensive list of donations totaling $230 million has been exposed. This extensive revelation encompasses a wide array of recipients, including friends, family, politicians, political action committees (PACs), and special interest groups.

Jasper

JasperAll prosecutors, regardless of their specific task force, receive basic training related to technology-related crimes and digital evidence. Task force-specific prosecutors are available to provide specialised expertise as required.

Davin

DavinReddit has announced the discontinuation of its blockchain-based rewards initiative, Community Points. The decision, outlined by Tim Rathschmidt, Reddit's director of consumer and product communications, comes as a response to the escalating challenges in scaling the program, exacerbated by evolving regulatory conditions.

JasperBaidu's innovative stride towards global AI competence and advancement, paving the way for China's technological aspirations.

Hui Xin

Hui XinBinance had previously suspended dollar deposits in June, following pressure from the SEC.

ClementReddit to phase out Community Points — The blockchain-based program that was designed to reward creators and developers on the platform.

Aaron