AB DAO 官方 Twitter 账号升级,提醒社区注意风险

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

Alex

Alex

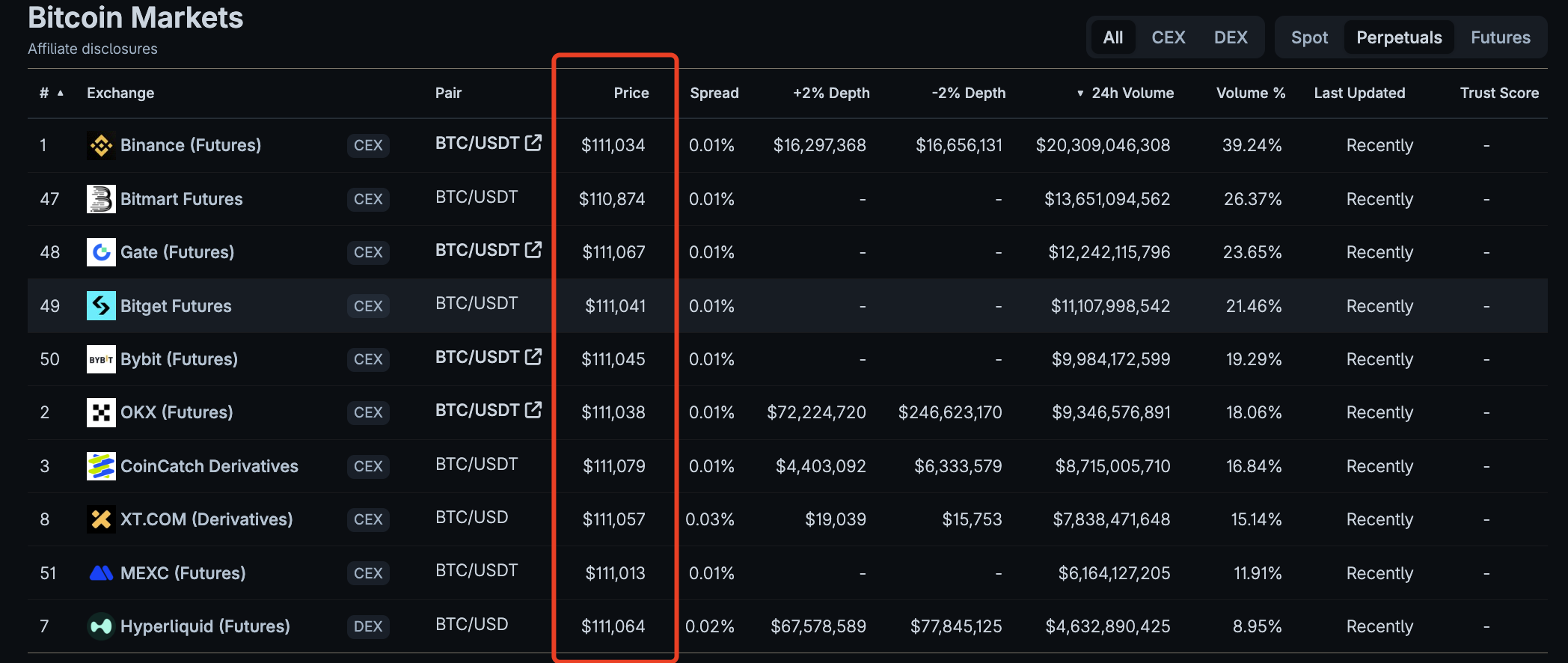

Looking at the BTC perpetual contract price chart above, you'll notice that none of the quotes from the top ten exchanges by trading volume are identical.

The current crypto market is highly fragmented: hundreds of centralized exchanges and thousands of decentralized protocols, with prices fragmented by each other. Coupled with the fragmented cross-chain ecosystem and the dominance of leveraged derivatives, investors face a difficult task in finding a transparent and fair trading environment. You may be wondering why I’m raising this question now. Because on September 18, the U.S. Securities and Exchange Commission (SEC) will hold a roundtable meeting on the prohibition of trade penetration to discuss its pros and cons and whether it should remain in the National Market System (NMS). This incident seems to be only related to traditional securities, but in my opinion, it also reminds the crypto market: If the trading protection mechanisms in the highly concentrated and mature rules of the U.S. stock market need to be reflected and upgraded, then in the more fragmented and complex crypto market, ordinary users need the most basic protection line even more: Crypto market providers (including CEX and DEX) must never ignore the better public prices at any time and must not allow investors to be traded at a bad price when this could have been avoided. Only in this way can the crypto market move from its "Wild West" state to true maturity and credibility. This may seem like a fantasy now, or even a pipe dream. However, when you understand the benefits that a no-trade-through rule would bring to the US stock market, you'll understand that, no matter how difficult, it's worth a try. 1. How was the no-trade-through rule established? Looking back, the establishment of this rule went through a complete chain of events: from legislative authorization in 1975, to the interconnectedness experiment of the Interexchange Trading System (ITS), to the full electronic transition in 2005, and finally, the phased implementation in 2007. It's not about eliminating volatility, but about ensuring that, even amidst volatility, investors still receive the better prices they deserve. 1.1 From Fragmentation to a Unified Market In the 1960s and 1970s, the biggest problem facing the US stock market was fragmentation. Different exchanges and market-making networks operated independently, leaving investors with no certainty about where to get the "best price at the moment." In 1975, the US Congress passed the Securities and Exchange Commission Amendments Act, which for the first time explicitly proposed the establishment of a "National Market System (NMS)" and mandated that the SEC lead the development of a unified framework that would connect various trading venues, with the goal of improving fairness and efficiency [Congressional website, sechistorical.org]. With legal authorization, regulators and exchanges launched a transitional "interconnection cable"—the Interexchange Trading System (ITS). Like a dedicated network cable connecting exchanges, it allows different venues to share quotes and routes, preventing better prices from being overlooked when transactions are completed at a lower price at one venue. [SEC, Investopedia] Although ITS gradually faded with the rise of electronic trading, the concept of "never ignoring the best price" has taken root. 1.2 Regulation NMS and Order Protection In the 1990s, the internet and decimalization made trading faster and more fragmented, and the old semi-manual system could no longer keep up. In 2004–2005, the SEC introduced a historic new regulation—Regulation NMS. It includes four core provisions: fair access (Rule 610), prohibition of trade penetration (Rule 611), minimum quotation unit (Rule 612), and market data rules (Rule 603) [SEC].

Among them, Rule 611 is also known as the "order protection rule." In plain words, it means that when a better protected quote has been posted elsewhere, you cannot match an order at a worse price. The so-called "protected quotes" must be quotes that can be executed immediately and automatically, and cannot be slow orders processed manually [SEC Final Rule].

To ensure the implementation of this rule, the US market has also established two key "foundations":

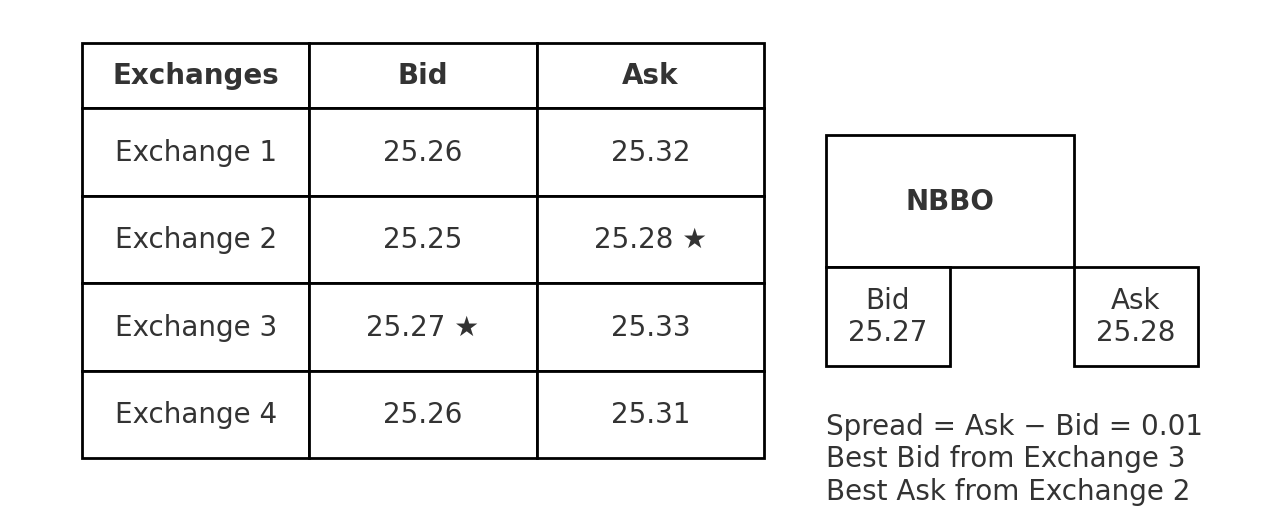

NBBO (National Best Bid and Offer): This combines the best bid and best ask prices across all exchanges to form a unified standard for measuring "penetration." For example, in the image above, 25.27 on Exchange 3 is the best bid, and 25.28 on Exchange 2 is the best ask.

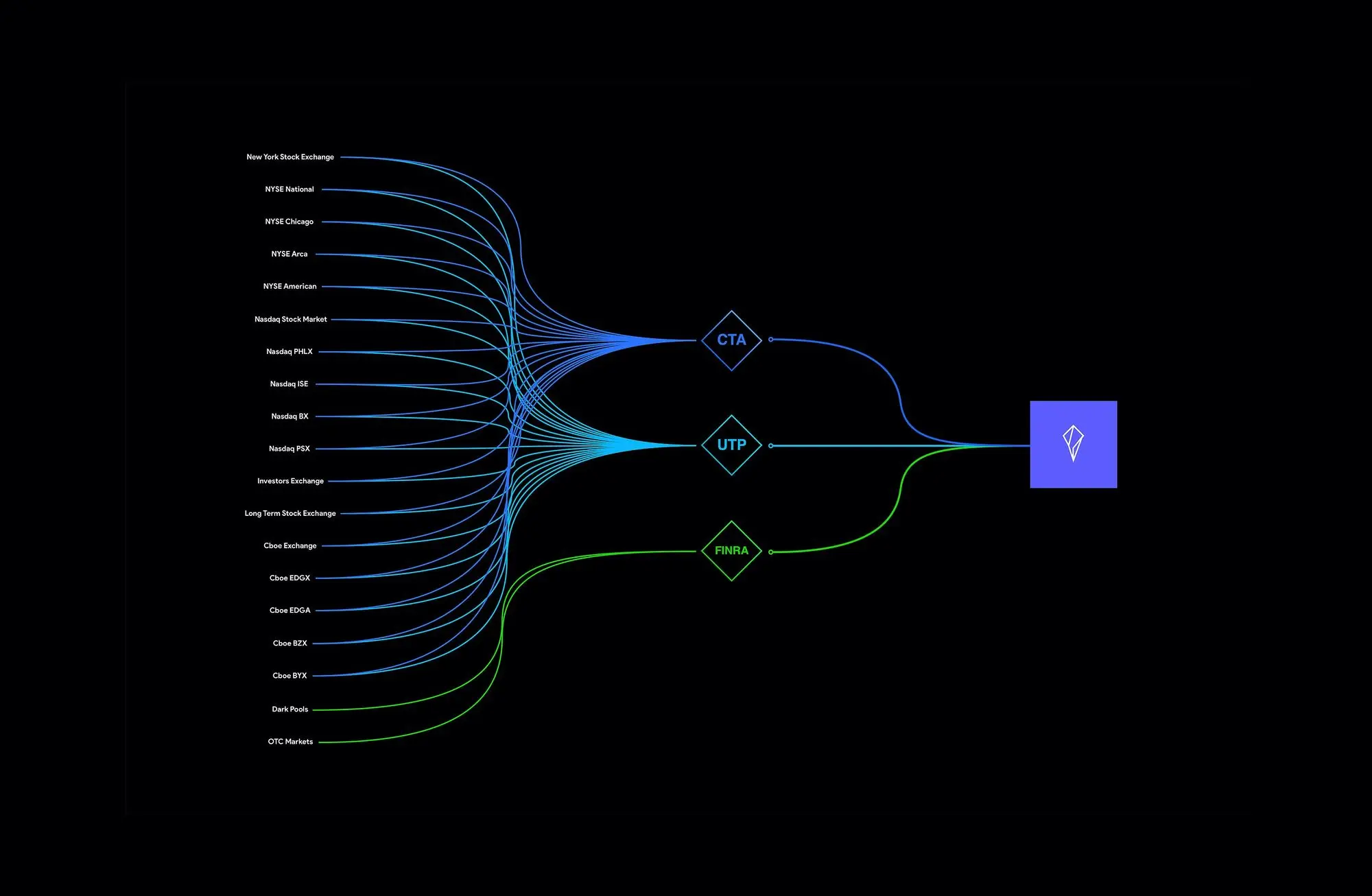

The SIP (Securities Information Processor, as shown above) is responsible for aggregating and publishing this data in real time, becoming the "single source of truth" for the entire market [Federal Register, SEC].

Reg NMS (Regulation National Market System) came into effect on August 29, 2005, and Rule 611 was first implemented on 250 stocks on May 21, 2007. It was fully extended to all NMS stocks on July 9 of the same year, eventually forming an industry-wide "no penetration of the better price" operating practice [SEC]. Of course, this has not been smooth sailing. SEC Commissioners Glassman and Atkins raised objections, arguing that focusing solely on display prices could ignore the net costs of transactions and even undermine market competition [SEC Dissent]. Yet, the majority of commissioners still supported the rule, and the reasoning was clear: despite the debate over cost and efficiency, prohibiting trade penetration at least ensures a fundamental bottom line: investors won't be forced to accept a worse price when a better one is readily available. This is why, to this day, Rule 611 is still considered one of the cornerstones of the "best execution ecosystem" in the US securities market. It transformed the principle of "better prices cannot be ignored" from a slogan into a practical rule that can be audited and held accountable. This bottom line is precisely what the crypto market lacks, yet it is the most valuable lesson to learn from. 2. Why does the crypto market need this "bottom line rule" even more? Let's get the point straight: in the crypto market, when you place an order, there isn't necessarily someone "looking around" for you. Different exchanges, chains, and matching mechanisms are like isolated islands, each with its own price. The result is that even when a better price is available elsewhere, you're "matched" to a worse price. This is explicitly prohibited in the US stock market by Rule 611, but there's no unified "safeguard" in the crypto world. 2.1 The Cost of Fragmentation: Lack of a "Full View" makes it easier to trade at a poor price. Currently, there are thousands of registered crypto trading venues worldwide: CoinGecko's "Global Chart" alone tracks over 1,300 exchanges (see the image below); and CoinMarketCap's spot trading chart consistently shows over 200 exchanges actively reporting volume—and this doesn't include the long tail of derivatives and on-chain DEXs. This landscape means no one has a natural view of the "best price across the board." Traditional securities rely on the SIP/NBBO combination to produce a "best price band." In crypto, however, an official combined price band doesn't exist. Even data providers bluntly state that "crypto has no 'official CBBO.'" This makes determining "where prices are cheaper/more expensive" a matter of hindsight. (CoinGecko, CoinMarketCap, coinroutes.com) 2.2 Derivatives Dominate, Amplifying Volatility: Cash outs are more likely to occur and have a greater impact. Derivatives have long accounted for the majority of crypto trading. Multiple monthly industry reports show that the proportion of derivatives fluctuates consistently between 67% and 72%. For example, a series of CCData reports have shown figures of 72.7% (March 2023), ~68% (January 2025), and ~71% (July 2025).

The higher the proportion, the more likely it is that instantaneous extreme prices ("spikes") will occur due to high leverage and funding rates; once your platform does not compare prices or calculate the net price, it may be "dealt on the spot" at a low price at the same time that a better price is available.

On the chain, MEV (maximum extractable value) is superimposed with a layer of "hidden slippage":

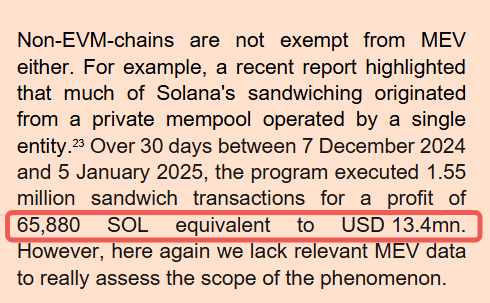

According to the European Securities and Futures Authority (ESMA) 2025 report, in the 30 days from 2024/12 to 2025/1 alone, there were 1.55 million sandwich transactions, with a profit of 65,880 SOL (about 1,340 Academic statistics also show over 100,000 such attacks per month, with associated gas costs in the tens of millions of dollars. For ordinary traders, these represent real “execution losses.” (CoinDesk Data, CryptoCompare, The Defiant, CryptoRank, arXiv)

If you want to understand how the MEV attack happened, you can read my article "A Complete Analysis of the MEV Sandwich Attack: The Fatal Chain from Sorting to Flash Exchange", which details how a MEV attack caused traders to lose $215,000.

The good news is that the market has developed some native technologies for "self-rescue":

Aggregation and smart routing (such as 1inch, Odos) will scan multiple pools/chains, split orders and calculate gas and slippage into the "real transaction cost" in an effort to get a better "net price"; (portal.1inch.dev, blog.1inch.io)

Don't be intimidated by the lack of an official market chart—there are already prototypes of "consolidated price charts" in the private sector.

CoinRoutes RealPrice/CBBO: CoinRoutes RealPrice/CBBO: CoinRoutes RealPrice synthesizes the depth, fees, and quantity constraints of over 40 exchanges in real time to create a tradable consolidated best price. Cboe signed an exclusive license for this product in 2020 for use in digital asset indices and benchmarks. In other words, “routing dispersed prices to better net prices” is mature in engineering. (Cboe Global Markets, PR Newswire)

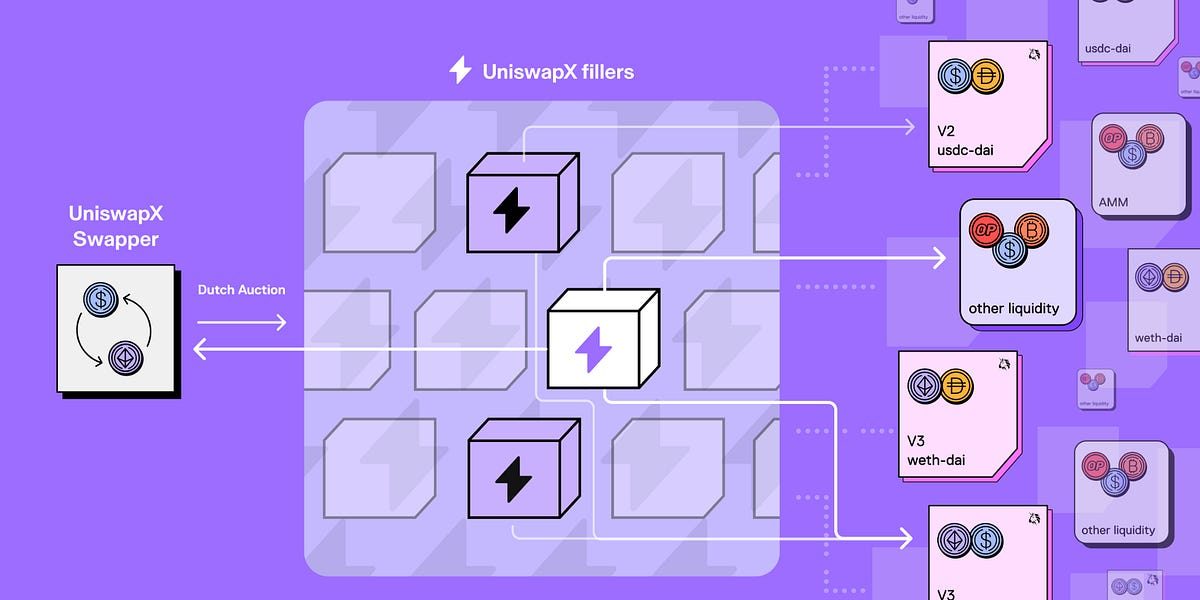

Aggregators and smart routers (as shown above): They can split orders, find paths across pools/cross chains, and calculate Gas and slippage into the actual transaction costs; UniswapX further uses auctions/intentions to aggregate on-chain and off-chain liquidity, bringing zero failure cost, MEV protection, scalable cross-chain capabilities, and is essentially pursuing "verifiable better net prices." (blog.1inch.io, portal.1inch.dev, Uniswap documentation) 3.3 The third step is to look at the rules: Don’t force a “bus”; establish “bottom line principles.” Unlike the US stock market, we will not force a global SIP, but will advance it in three tiers: Principles first (same compliance circle): Establish a clear obligation among compliant platforms/brokers/aggregators in a single jurisdiction not to penetrate the better public price/net price. What is the "net price"? Don't just look at the nominal price on the screen; take into account fees, rebates, slippage, gas, and failed retry costs. Article 78 of the EU's MiCA has already codified the "best outcome" into a statutory list (price, cost, speed, execution and settlement possibilities, scale, custody conditions, etc.); this principled approach can serve as the anchor for "encrypted anti-penetration." (esma.europa.eu, wyden.io) Market-based consolidated price bands + spot checks and verification: Regulators recognize multiple private "consolidated price bands/reference net prices" as a compliance baseline, such as the aforementioned RealPrice/CBBO. The key isn't to designate a "single data source," but rather to require transparent methodology, disclosure of coverage, conflict resolution, and random comparisons/external spot checks. This prevents a single dominant player while providing practitioners with a clear, verifiable benchmark. (Cboe Global Markets) "Best Execution Certification" and Periodic Reconciliation: Platforms and brokers must maintain records of which venues/routes were searched, why a better notional price was abandoned (e.g., settlement uncertainty, excessive gas), and the difference between the final net transaction price and the estimated price. Similar to traditional securities, FINRA Rule 5310 requires "order-by-order or 'regular and rigorous'" execution quality assessments (at least quarterly and by category). Cryptocurrency should also adopt the same level of self-certification and disclosure. (FINRA) 3.4 The fourth step is to consider boundaries: Innovation should not be "stuck." The principle is "not to disregard the better public price," but the path to achieving it must be technology-neutral. This is also the lesson from the recent US Rule 611 roundtable: even in the highly concentrated US stock market, order protection is being reconsidered, and a one-size-fits-all approach is even more unacceptable in crypto. (U.S. Securities and Exchange Commission, Sidley) So, what will this look like in practice? Here's a visual example (imagine it): You place an order on a compliant CEX/aggregator. The system first queries multiple venues/chains/pools, using a private consolidated price band as a reference. For each candidate path, the system factors in fees, slippage, gas, and expected finality time. If a path has a better nominal price but falls short of finality/fees, the system clearly documents the reason and retains evidence. The system selects the path with the better overall net price and a timely execution time (splitting the order if necessary). If it doesn't route you to the better net price at the time, subsequent reports will flag a red flag, creating a compliance risk. If caught in a spot check, an explanation or even compensation will be required. You'll see a concise execution report: best available net price vs. actual net price, path comparison, estimated and actual slippage/fees, transaction time, and on-chain finality. Even the most naive traders can use this to determine: "Am I being underpriced?" Finally, let's address the concerns: "Can't we operate without a global NBBO?" Not necessarily. MiCA has already implemented the "best execution" principle for cryptographic service providers (CASPs), emphasizing multiple factors such as price, cost, speed, and execution/settlement probability. The traditional self-certification and spot check system used in US stocks can also be applied. By using multiple consolidated price bands + audit reconciliation, a "consensus price band" can be established, rather than forcing out a "central tape". (esma.europa.eu, FINRA)

“There is MEV on the chain, will I still be subject to slippage?” This is exactly the problem that protocols such as UniswapX (as shown above) aim to solve: MEV protection, zero cost of failure, cross-source bidding, and returning the margin originally taken away by “miners/sorters” as price improvements as much as possible. You can think of it as a "technical version of order protection." (Uniswap documentation, Uniswap) Conclusion in one sentence: The path to implementing "anti-penetration" in the cryptocurrency market isn't to replicate the machine-like rules of the US stock market. Instead, it's to anchor it in principles and obligations at the MiCA/FINRA level, combining private merger price bands with on-chain verifiable "best execution certificates." Starting within the same regulatory perimeter, then gradually expanding outward. By making "better public prices cannot be ignored" an auditable and accountable commitment, even without a "global bus," we can mitigate the damage caused by "pin-splitting" and recover as much of the money retail investors deserve from the system as possible. Conclusion | Turning "Best Price" from a Slogan into an Institution The crypto market has no shortage of clever code; what it lacks is a bottom line that everyone must adhere to. Banning transaction penetration isn't about tying down the market, but about streamlining responsibilities: platforms must either send you to a better net price or provide verifiable reasons and evidence. This doesn't restrict innovation; rather, it paves the way for it. When price discovery is fairer and execution more transparent, truly efficient technologies and products will be amplified. Stop treating "spikes" as the market's destiny. What we need is a technology-neutral, verifiable, and layered approach to cryptographic "order protection." Turn "better prices" from a possibility into an auditable promise. Only when better prices are "not ignored" can the crypto market be considered mature.

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

AlexGoogle Cloud’s new Blockchain RPC service simplifies Ethereum-based DApp development, offering scalable solutions to address the growing needs of Web3 developers.

Sanya

SanyaArweave, Arweave's working principle and significance of existence Golden Finance, this article briefly introduces Arweave's working principle and value.

JinseFinance

JinseFinanceOn August 8, the U.S. Federal Reserve took a major enforcement action against Pennsylvania-based Customers Bank, marking the U.S. government’s gradual increase in regulatory oversight of cryptocurrency-related businesses.

JinseFinanceVitalik Buterin reveals Ethereum's simplification plan, "The Purge," aimed at reducing historical data storage and addressing technical debt. Initiatives include EIPs, Geth cleanup, and introducing SSZ. Concerns raised over complex Layer 2 scaling solutions, emphasizing a balanced approach.

Xu Lin

Xu LinWeb3Auth launches 'Wallet Services,' aiming to streamline web3 development with pre-built templates and introduces 'Pregenerated Wallets' for simplified user engagement.

Joy

JoyThese offerings, christened "Gas Station" and "Smart Contract Platform," promise to usher in an era of enhanced convenience and cost-efficiency.

CatherineJinseFinance

CatherineJinseFinanceNigel Dobson, head of portfolio banking services at ANZ, said: "When we looked at this in depth, we came to the conclusion that this is a significant protocol shift in financial market infrastructure."

Cointelegraph

Cointelegraph"We could be exposed to reputational risks brought by DT service providers created in Singapore, and which provide services relating to virtual assets," said Alvin Tan.

Cointelegraph