Author: imToken

"Derivatives are the holy grail of DeFi." As early as 2020, the market had reached a consensus that on-chain perp protocols were DeFi's ticket to the second half.

But the reality is that over the past five years, whether limited by performance or cost, perp DEXs have always made a difficult trade-off between "performance" and "decentralization." During this period, the AMM model represented by GMX, while achieving permissionless trading, could hardly match CEX in terms of transaction speed, slippage, and depth. Until the emergence of Hyperliquid, leveraging its unique on-chain order book architecture, it achieved a smooth CEX-like experience on a fully self-hosted blockchain. The recently approved HIP-3 proposal has further torn down the barriers between crypto and tradfi, opening up endless possibilities for trading a wider range of assets on-chain. This article will also provide an in-depth analysis of Hyperliquid's operating mechanisms and revenue streams, objectively analyze its potential risks, and explore the revolutionary changes it brings to the DeFi derivatives market. The Perp DEX Cycle: Leverage is a core primitive in finance. In mature financial markets, derivatives trading far surpasses spot trading in terms of liquidity, capital volume, and transaction scale. After all, through margin and leverage mechanisms, limited funds can leverage a larger market volume, meeting diverse needs such as hedging, speculation, and yield management. This trend has been borne out in the crypto world, at least within the CEX sector. As early as 2020, CEX derivatives trading, represented by futures contracts, began to replace spot trading, gradually becoming the dominant market. Coinglass data shows that over the past 24 hours, the daily trading volume of futures contracts on leading CEXs has reached tens of billions of dollars, with Binance exceeding $130 billion.

Source: Coinglass

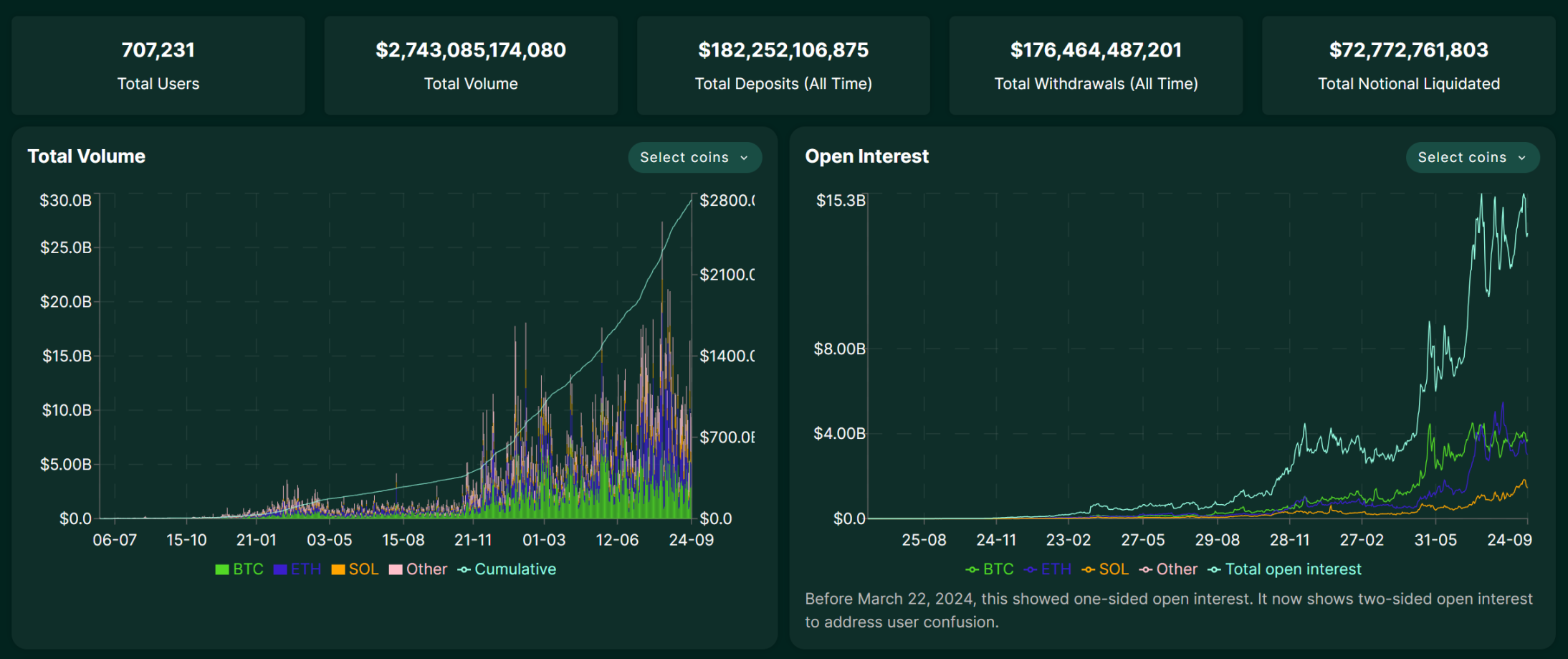

In contrast, on-chain perp DEX has been a long journey of five years. During this period, dYdX explored a more centralized experience through on-chain order books, but faced challenges in balancing performance and decentralization. Although the AMM model represented by GMX has achieved permissionless transactions, it is still far behind CEX in terms of transaction speed, slippage and depth. In fact, the sudden collapse of FTX in early November 2022 briefly stimulated a surge in trading volume and new users for on-chain derivatives protocols like GMX and dYdX. However, due to constraints in the market environment, on-chain trading performance, trading depth, trading variety, and other comprehensive trading experiences, the entire sector quickly fell into silence again. To be honest, once users discover that on-chain trading carries the same risk of liquidation but lacks the liquidity and experience of CEXs, their willingness to migrate naturally diminishes. Therefore, the key issue isn't whether there's demand for on-chain derivatives, but rather the continued lack of a product that can both provide irreplaceable value to CEXs and address performance bottlenecks. The market gap is clear: DeFi needs a perp DEX protocol that truly delivers a CEX-level experience. It's against this backdrop that the emergence of Hyperliquid has brought a new dimension to the entire market. What's less well-known is that, while Hyperliquid only officially debuted and entered the public eye this year, it was actually launched as early as 2023, with continuous iteration and development over the past two years. Is Hyperliquid the ultimate form of "on-chain CEX"? Facing the long-standing "performance vs. decentralization" dilemma in the per-DEX space, Hyperliquid's goal is straightforward: to replicate the smooth CEX experience directly on-chain. To this end, it has chosen a radical approach. Rather than relying on the performance constraints of existing public chains, it has built its own dedicated Layer 1 application chain based on the Arbitrum Orbit technology stack, integrating a fully on-chain order book and matching engine. This means that all transaction steps, from order placement to matching to settlement, occur transparently on-chain, achieving millisecond processing speeds. Architecturally, Hyperliquid resembles a "fully on-chain version" of dYdX, no longer relying on any off-chain matching, aiming directly at the ultimate form of an "on-chain CEX." This radical approach has been immediately effective. Since the beginning of this year, Hyperliquid's daily trading volume has steadily climbed, reaching $20 billion at one point. As of September 25, 2025, its cumulative total trading volume has exceeded $2.7 trillion, surpassing even most second-tier CEXes in revenue. This clearly demonstrates that the problem with on-chain derivatives isn't a lack of demand, but rather a lack of product forms truly suited to the characteristics of DeFi.

Source: Hyperliquid

Of course, such strong growth has also quickly brought it ecological attraction. The recent bidding war for USDH issuance rights launched by HyperLiquid is the best example, which attracted heavyweight players such as Circle, Paxos, and Frax Finance to openly compete (further reading: "Starting from HyperLiquid's USDH becoming a hot commodity: What is the fulcrum of DeFi stablecoins?"). However, simply replicating the CEX experience isn't the endgame for Hyperliquid. The recently approved HIP-3 proposal introduces permissionless, developer-deployed perpetual contract markets to the core infrastructure. Previously, only the core team could list trading pairs, but now anyone who stakes 1 million HYPE can deploy their own markets directly on-chain. In short, HIP-3 allows the permissionless creation and listing of derivatives markets for any asset on Hyperliquid. This completely breaks the limitation of Perp DEX, which previously only traded mainstream cryptocurrencies. Under the framework of HIP-3, in the future we may see on Hyperliquid:

Stock market: trading Tesla (TSLA), Apple (AAPL) and other global financial market top assets;

Commodities and foreign exchange: trading traditional financial products such as gold (XAU), silver (XAG) or euro/dollar (EUR/USD);

Prediction market: betting on various events, such as "whether the Federal Reserve will cut interest rates next time" and "the floor price of a blue-chip NFT".

This will undoubtedly greatly expand Hyperliquid's asset categories and potential user base, blurring the lines between DeFi and TradFi. In other words, it allows any user globally to access core assets and financial methods in a decentralized, permissionless manner. What's the other side of the coin? While Hyperliquid's high performance and innovative model are exciting, they also carry significant risks, especially given that it hasn't yet undergone the stress test of a major crisis. The cross-chain bridge issue is the primary concern and a frequently discussed topic in the community. Hyperliquid connects to the mainnet via a cross-chain bridge controlled by a 3/4 multi-signature, creating a centralized trust node. If these signatures fail, either accidentally (e.g., private key loss) or maliciously (e.g., collusion), the security of the assets of all users on the bridge is directly threatened. Secondly, there's the risk of the treasury strategy, as the returns on the HLP treasury are not guaranteed. If the market maker's strategy incurs losses under certain market conditions, the principal deposited in the vault will also be reduced. While users enjoy the prospect of high returns, they also bear the risk of strategy failure. As an on-chain protocol, Hyperliquid also faces common DeFi risks, such as smart contract vulnerabilities, oracle price feed errors, and user liquidations in leveraged trading. In fact, in recent months, the platform has experienced multiple large-scale liquidations in extreme market conditions due to malicious price manipulation of some small-cap cryptocurrencies, highlighting its need for improvement in risk control and market regulation. Furthermore, objectively speaking, there is another issue that many people have not considered publicly: as a rapidly growing platform, Hyperliquid has yet to undergo major compliance audits or serious security incidents. During a platform's rapid expansion, risks are often overshadowed by the halo of rapid growth. Overall, the story of perp DEX is far from over. Hyperliquid is just the beginning. Its meteoric rise demonstrates both the genuine demand for on-chain derivatives and the feasibility of overcoming performance bottlenecks through architectural innovation. HIP-3 extends this imagination to stocks, gold, foreign exchange, and even prediction markets, truly blurring the lines between DeFi and TradFi for the first time. While high returns always come with high risks, from a macro perspective, the appeal of the DeFi derivatives track will not diminish due to the risks of a single project. It's not impossible that other projects will emerge in the future to take over from Hyperliquid/Aster and become the next leading on-chain derivatives projects. Therefore, as long as we believe in the allure and potential of the DeFi ecosystem and derivatives track, we should pay close attention to these promising players. Perhaps years from now, we will look back and see this as a brand new historical opportunity.

Anais

Anais