On May 21, the Legislative Council of Hong Kong officially passed the Stablecoin Bill (hereinafter referred to as the "Bill"). The news was overwhelming, so I will not go into details. In summary, there are a few points:

• Hong Kong allows the issuance of stablecoins

• A license needs to be applied for, with a threshold of 25 million Hong Kong dollars

• Stablecoins need to be anchored to legal currency, and Hong Kong will implement supervision

• The regulations are expected to take effect in 2025

The passage of the "Bill" is undoubtedly a bombshell in the circle. Will this lead to a reshuffle in the currency circle? How will it affect the cross-border payment landscape? How should you and I, as ordinary people, respond?

What is a stablecoin?

Perhaps you don't know about stablecoins, but you must have heard of Bitcoin. Bitcoin is a virtual currency issued on the blockchain, which is characterized by decentralization, immutability, and information transparency. Based on the consensus mechanism of the blockchain, technologies such as smart contracts have also been born.

The many pros and cons of Bitcoin are not within the scope of this article. With the help of various parties, its price has been rising all the way, and it has also fallen sharply in a short period of time. In short, it is too unstable. So people want to find a cryptocurrency that has both the advantages of Bitcoin and a relatively stable price, and stablecoins came into being.

Stablecoins are still issued based on blockchains, but the difference is that the price is stable. This stability is achieved based on a certain mechanism, either anchoring to legal currency (such as USDT anchoring to the US dollar), or maintaining the stability of the currency value through algorithms. The Draft stipulates that stablecoins must be anchored to legal tender, which directly denies the legitimacy of algorithmic coins.

How will stablecoins impact the traditional payment industry

The traditional payment industry has always had several pain points:

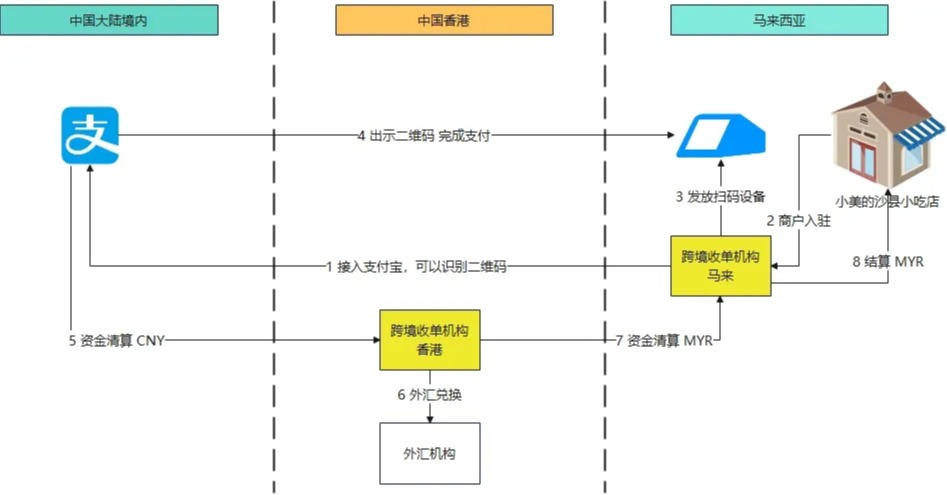

1. It is impossible to achieve real-time settlement of funds. Funds are from China->Hong Kong->Malaysia. After receiving CNY, the "cross-border acquiring institution-Hong Kong" must wait for the payment channel to clear funds (usually T+1). After receiving CNY, it will exchange foreign currency and then settle it to the "acquiring institution-Malaysia". Finally, it will be settled to the merchant, which can be as fast as T+5 or as slow as T+10. The timeliness of funds arriving is poor.

2. The cost of funds is high. Cross-border fund settlement cannot be separated from the participation of SWIFT. Of course, SWIFT needs to charge fees. In addition, foreign exchange institutions and intermediary banks also need to charge fees. The more nodes a fund channel passes through, the higher the cost

3. Fund security has always been a difficult problem to solve. You must identify the risk of "error, omission, duplication and delay" of funds yourself. You should assume that every participant in cross-border payments may have "problems" and establish an effective prevention and control mechanism.

Advantages of stablecoins:

1. Compared with traditional payment and settlement, cryptocurrency has significantly improved the timeliness of account arrival, and theoretically it can be reached in seconds.

2. Without middlemen to make a profit from the price difference, the cost of funds has plummeted (there are still middlemen, such as exchanges, cross-chain transactions, etc., but they are much lower than the rates of traditional payments)

3. Smart contract technology based on blockchain cannot be tampered with or denied, which provides another solution for fund security

4. Stablecoin/cryptocurrency payment will be the underlying infrastructure of Web 3.0

Challenges faced by stablecoins

Although we can see many prospects for stablecoins, they also have some problems that restrict their further development:

• Although blockchain is transparent, the management of stablecoins may not be transparent. For example: Has sufficient reserve been paid for issuing stablecoins? Is there a risk of misappropriation of reserve funds?

• The acceptance and recognition of stablecoins in the market are still not high enough. The scenarios that can directly support stablecoin payments are relatively limited. Even after receiving stablecoins, merchants still need to convert them into legal currency before they can use them.

• They may be used in the black and gray industrial chain to circumvent foreign exchange controls and threaten the stability of the financial system.

• They are heavily dependent on the stability and security of the blockchain infrastructure.

I have always believed that technical issues are not the main contradiction and will be resolved soon, but other aspects are very dependent on the soundness and improvement of regulatory policies.

In addition, it may be a long process for stablecoins to gain the trust of the public, which requires governments, major cross-border institutions, merchants, and underlying infrastructure to work together simultaneously.

Current attitudes of various countries towards stablecoins The United States

The United States has been repeatedly defeated in diplomacy recently, and the tariff stick does not seem to be so useful. However, in the stablecoin market, the market value of USDT and USDC anchored to the US dollar is far ahead, and the United States is eager to use this to establish a new monetary hegemony.

On May 19 this year, the GENIUS Stablecoin Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) has been advanced to the voting stage. This means that further compliance of stablecoins has finally been put on the agenda. Although it still needs to be voted through and signed by the president before it can officially take effect, it is only a matter of time.

European Union

The European Union officially passed MiCA (Markets in Crypto-Assets Regulation) in 2024 as the first comprehensive regulatory framework formulated by the European Union to regulate the crypto asset market.

MiCA subdivides crypto assets into asset reference tokens (ARTs), electronic money tokens (EMTs), and other crypto assets, and adopts differentiated regulatory strategies. The provisions related to stablecoins will officially take effect on June 30, 2024.

Singapore

The Monetary Authority of Singapore (MAS) issued the "Stablecoin Regulatory Framework" in August 2023, which clearly included single-currency stablecoins (SCS) anchored to the Singapore dollar or G10 currencies (such as the US dollar, euro, yen, etc.) within the scope of supervision.

In 2025, stablecoins will be further classified as digital payment tokens (DPTs), which must comply with the revised Payment Services Act (PSA).

As one of the financial centers in Asia, Singapore has always been at the forefront of innovation, and the value of MAS's license is still increasing.

China

Because of the risks of cryptocurrencies, the Eastern giant has always been cautious about cryptocurrencies. At present, the Eastern giant has not officially recognized the legality of any cryptocurrency.

However, this currency war has quietly started, and not participating means falling behind. Therefore, as a financial free port, it is a very appropriate time for Hong Kong to pass the "Draft" at this time. It can not only stabilize its position as an Asian financial center, but also explore some experience in the promotion and operation of stablecoins. Whether the Eastern giant's attitude towards cryptocurrencies will change in the future may largely depend on the results of Hong Kong's experiments.

After the "Draft" was passed, JD.com and Standard Chartered Bank have entered the first batch of sandbox testing phases and started to apply for regulatory licenses at the same time.

I am quite surprised by JD.com’s layout on stablecoins. After all, the two major domestic payment giants seem to have not started to move yet. But I think it should be soon. Let’s wait and see.

How should ordinary people deal with it?

Opportunities often coexist with challenges. If ordinary people want to get involved, there may be a few suggestions for reference:

• Invest in stablecoins? It is recommended not to consider it in the short term. Stablecoins are anchored to legal currency. If you have this idea, you might as well deposit some foreign exchange directly

• Opportunities in cross-border payments. If you are a cross-border payment practitioner, you can consider and explore the feasibility of stablecoin payments, but you must pay close attention to policy trends. In Hong Kong, it is better to wait until the "Draft" is actually implemented

• Issue stablecoins yourself? This is not something that ordinary people should consider. If you are interested, you can try NFT.

• If ordinary people want to get involved, the easiest way is to find a Web 3.0 company to work.

Finally, it is recommended to pay attention to the trends of digital RMB and CISP. Using digital RMB to connect stable currency and go global is the ultimate move of the Eastern power.

The wheel of history rolls forward, and the rise of Web 3.0 has become an unstoppable trend. Who can compete in this new revolution? Let's wait and see.

Weiliang

Weiliang