Author: @Web3Mario

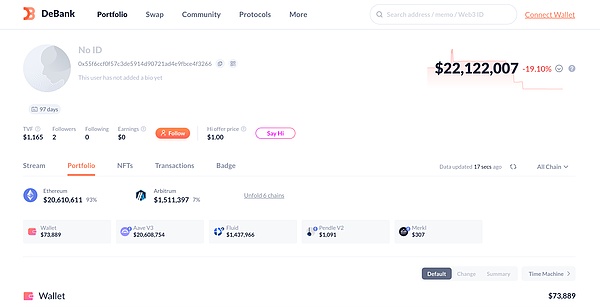

Abstract: With recent regulatory changes, DeFi protocols, leveraging on-chain traders' enthusiasm for crypto assets, have achieved significantly higher interest rates than traditional financial models. This has positive implications for two groups of users. First, for some traders, after most blue-chip crypto assets have reached record highs, appropriately reducing leverage and seeking out low-alpha investment scenarios is a good option. Furthermore, with the macroeconomic environment entering a cycle of interest rate cuts, non-crypto professionals can also enjoy higher returns by allocating their idle assets in DeFi. Therefore, I would like to start a new series of articles to help everyone quickly get started with DeFi. By analyzing the returns and risks of different strategies using real-world data from DeFi whales, I hope you will support me. In this first installment, I will begin with the recently popular interest rate arbitrage strategy and analyze its opportunities and risks using the capital allocation of major AAVE traders. What are the typical scenarios for interest rate arbitrage in the DeFi world? First, for those unfamiliar with finance, let's explain what interest rate arbitrage is. Interest rate arbitrage, also known as carry trade, is a financial arbitrage strategy that exploits interest rate differences between different markets, currencies, or debt instruments to profit. Simply put, this strategy follows a simple path: borrow at a low interest rate, invest at a high interest rate, and profit from the interest rate differential. In other words, arbitrageurs borrow funds at a low cost and then invest them in higher-yielding assets, profiting from the interest rate differential. For example, the US-Japan carry trade is a popular strategy among hedge funds in traditional financial markets. As we know, Japan's YCC policy has consistently maintained extremely low bond interest rates, with real interest rates even at negative levels. Meanwhile, the US dollar remains at a high interest rate, resulting in an interest rate differential between the two financing markets. Hedge funds use U.S. Treasuries, a high-interest-bearing asset, as collateral to borrow yen from various financing channels. They then either purchase high-dividend-yielding assets from Japan's five largest trading companies or convert the funds back into U.S. dollars to purchase other high-return assets. (PS: One of Buffett's favorite strategies.) This strategy benefits from increased leverage. The scale of this arbitrage path alone is sufficient to influence global risk asset prices. This explains why, after the Bank of Japan abandoned the YCC, each interest rate hike over the past year has significantly impacted risk asset prices. In the DeFi world, the core innovations are divided into two broad categories: decentralized exchanges (DEXs), and decentralized lending protocols (Lending). The former promotes "spread arbitrage strategies," which we won't discuss in this article, while the latter is the primary source of "spread arbitrage strategies." Decentralized lending protocols enable users to use one crypto asset as collateral to borrow another. Specific classifications vary depending on liquidation mechanisms, collateralization requirements, and interest rate determination methods. However, without further elaboration, we'll focus on the most mainstream overcollateralized lending protocol in the current market to introduce this strategy. Using AAVE as an example, you can use any supported crypto asset as collateral to lend another crypto asset. During this process, your collateral still earns both the original yield and the platform's lending yield, which is represented by the Supply APY. This is because most lending protocols utilize a peer-to-pool model. Your collateral automatically enters a unified pool of funds, serving as the platform's lending source. Therefore, borrowers who demand your collateralized assets also pay interest to this pool, which is the source of the lending yield. You, however, pay the interest corresponding to your loaned assets, which is represented by the Borrow APY. These two interest rates are variable and, in AAVE, are determined by the interest rate curve. Simply put, the higher the utilization rate of the pool, the higher the corresponding interest rate. This design is due to the fact that in the Peer to Pool lending protocol, loans do not have a maturity date like in traditional financial markets. This simplifies the complexity of the protocol and provides lenders with higher liquidity, as they do not need to wait until the debt matures to retrieve their principal. However, to ensure sufficient repayment constraints on borrowers, the protocol requires that once the remaining liquidity in the pool decreases, the borrowing interest rate increases. This higher interest rate forces borrowers to repay, ensuring that the remaining liquidity in the pool is always in a dynamic equilibrium, which best reflects the true market demand. Now that we understand the basics, let's explain how interest rate arbitrage works. First, you need to find an asset with a higher native asset yield plus a higher Supply APY as collateral. Next, you need to find a suitable lending path with a lower Borrow APY to borrow the asset. Finally, you use the borrowed funds to purchase collateral again in the secondary market and repeat the above steps to increase your leverage. Anyone with financial common sense can easily spot two risks associated with this approach: 1. Exchange rate risk: If fund A depreciates relative to fund B, liquidation risk may arise. For example, if your collateral is ETH and your loan is USDT, a decline in ETH prices could result in insufficient collateralization, leading to liquidation. 2. Interest rate risk: If the Borrow APY of fund pool B is higher than the combined yield of fund pool A, the strategy is in a loss-making state. Liquidity Risk: The exchange liquidity between Funds A and B determines the establishment and exit costs of the arbitrage strategy. A significant drop in liquidity can still have a significant impact. To mitigate exchange rate risk, most DeFi interest rate arbitrage schemes require a certain correlation between the prices of the two funds, preventing significant deviations. Therefore, there are two main target options in this sector: the LSD path and the Yield-Bearing Stablecoin path. The difference depends on the underlying asset type of the managed funds. If the underlying asset type is risky, in addition to interest rate arbitrage, it can still maintain the ability to generate alpha returns on the native asset. For example, Lido uses stETH as collateral to lend ETH. This arbitrage path was very popular during the LSDFi Summer period. Another advantage of choosing a linked asset is higher maximum leverage. This is because AAVE sets a higher Max LTV for the linked asset, also known as E-Mode. At a 93% value setting, the theoretical maximum leverage is 14x. So based on the current yield rate, taking AAVE as an example, the lending yield rate of wsthETH is ETH's native yield of 2.7% + 0.04% Supply APY, while ETH's Borrow APY is 2.62%. This means there is a 0.12% interest rate spread, so the potential yield rate of this strategy is 2.74% + 13 * 0.12% = 4.3%. As for interest rate risk and liquidity risk, they can only be mitigated by continuously monitoring bilateral interest rates and related liquidity. Fortunately, this risk does not involve immediate liquidation, so only timely liquidation is required. How an AAVE whale used $10 million to earn a 100% APR through interest rate arbitrage. Next, let's take a look at how DeFi whales use interest rate arbitrage to achieve excess returns. As mentioned in a previous article, AAVE accepted PT-USDe, issued by Pendle, as collateral a few months ago. This has completely boosted the profitability of interest rate arbitrage. We can see on AAVE's official website that PT-USDe remains in a supply-capped state, which also demonstrates the popularity of this strategy. We selected the DeFi whale with the largest collateral in the market, 0x55F6CCf0f57C3De5914d90721AD4E9FBcE4f3266, to analyze his capital allocation and potential returns. This account has a total asset size of $22 million, most of which is used to allocate to the above strategies.

This account allocates funds across two lending markets: 20.6M in the AAVE ecosystem and 1.4M in Fluid. As the chart shows, this account leverages approximately 230M in PT-USDe assets using 20M principal in AAVE. The corresponding borrowing allocations are 121M USDT, 83M USDC, and 4M USDe. Next, let's calculate its APR and leverage ratio. According to the PT-USDe interest rate at the time of opening the position, the main lock-in rate occurred at 20:24 on August 15, which means that the account's opening interest rate was 14.7%. The current borrowing rate for USDT on AAVE is 6.22%, for USDC 6.06%, and for USDDe 7.57%. This gives a leverage ratio of 11.5x and a total return of 104%. These are very attractive numbers! How Can DeFi Newbies Replicate the Strategies of Experts? In fact, replicating this interest rate arbitrage strategy isn't difficult for a DeFi novice. Numerous automated interest rate arbitrage protocols already exist on the market, helping average users circumvent the complex underlying revolving loan logic and open positions with a single click. Since I'm speaking from a buyer's perspective, I won't mention specific projects here; you can find them on the market. However, I would like to point out the risks of this strategy, which can be categorized into three main areas: 1. Regarding exchange rate risk, a previous article has already introduced the AAVE official community's design logic for the PT asset oracle. Simply put, once the oracle is upgraded to capture changes in PT assets in the secondary market, the strategy will need to control leverage to avoid the risk of liquidation when the maturity date is long and the market price is volatile. 2. Regarding interest rate risk, users need to continuously monitor changes in interest rate spreads and adjust their positions immediately when spreads converge or even turn negative to avoid losses. 3. Regarding liquidity risk, this primarily depends on the fundamentals of the target interest-bearing asset project. If a major crisis of trust occurs, liquidity will quickly dry up, and the slippage losses suffered by the exit strategy will be significant. Users should also remain vigilant and keep an eye on the project's progress.

Kikyo

Kikyo