Tether CEO:USDT 受美国监管威胁,Tether承诺配合制裁要求

《华尔街日报》近日报道称,美国检察官正在调查 Tether 是否违反制裁和反洗钱法规,USDT 或被部分非法组织利用。Tether CEO 表示,公司致力于遵守国际制裁,不会与监管部门对抗。

Alex

Alex

Author of the article: Thejaswini M A Article compilation:Block unicorn

I used to be excited about every cryptocurrency financing announcement.

Every seed round of financing was like major news. “Anonymous team raises $5M for revolutionary DeFi protocol!” I’d frantically research the founders and dive into their Discords, trying to understand what was so special about this project. Fast forward to 2025. Another funding round pops up in my headlines. Series A. $36M. Stablecoin payments infrastructure. I filed it under “Enterprise Blockchain Solutions” and moved on to other things. When did I become so… pragmatic?

For the first time since 2020,

crypto venture capital late-stage deals have surpassed early-stage deals.

65% to 35%.

Read that again.

This industry was once built on pre-seed funding, with anonymous teams in garages building innovative DeFi protocols.

Now? Series A and beyond are driving the money.

What changed?

Everything has changed. And yet nothing seems to have changed.

VCs in suits. Due diligence has gone from minutes to months.

Regulatory compliance. Institutional adoption.

Professional project pitches, not anonymous Discord messages.

KYC processes. Legal teams. Real, meaningful revenue models.

Companies like Conduit raised $36M for “unified on-chain payments.” Beam raised $7M for “stablecoin-based payment services.”

These are infrastructure projects. B2B solutions. Enterprise-grade platforms.

Boring, profitable, scalable businesses.

Crypto VC headlines love to exaggerate numbers, so let’s start with the facts:

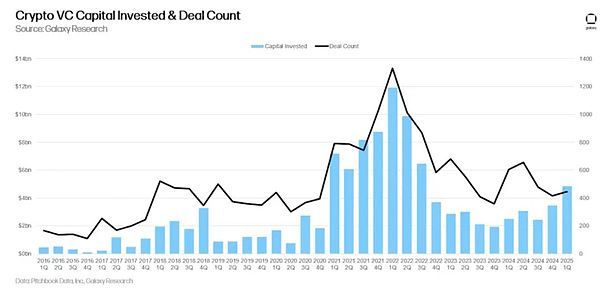

Q1 2025: $4.9 billion invested in 446 deals (up 40% QoQ).

Year-to-date: $7.7 billion raised, on track to reach $18 billion in 2025.

And here’s the thing:MGX (Abu Dhabi’s sovereign fund) wrote a $2 billion check to Binance.

This perfectly reflects the current venture capital environment: a handful of huge deals skew the data, while the overall ecosystem remains sluggish.

According to Galaxy Research, the correlation between Bitcoin’s price and VC activity — which had been reliable for years — broke down in 2023 and has yet to recover.

Bitcoin hits new highs, while VC activity remains sluggish.

It turns out that institutions don’t need to fund venture startups to gain exposure to crypto when they can buy a Bitcoin ETF. A Reality Check for Venture Capital Crypto venture investment falls 70% from a peak of $23 billion in 2022 to just $6 billion in 2024. The number of deals plummets from 941 in the first quarter of 2022 to 182 in the first quarter of 2025.

But this is the part that should scare every founder claiming “the next big thing” — of the 7,650 companies that raised seed rounds since 2017, only 17% made it to Series A.

And a mere 1% made it to Series C.

This is the maturation of crypto venture capital, and it’s going to be painful for those who thought the party would last forever.

The hot narratives of 2021-2022 — games, NFTs, DAOs — have all but disappeared from VC interest.

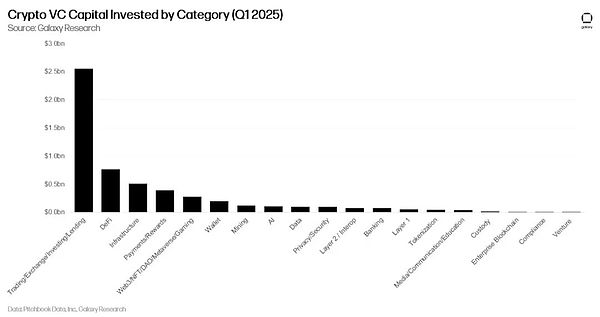

Companies building exchanges and infrastructure attracted the majority of VC funding in Q1 2025. DeFi protocols raised $763M. Meanwhile, the Web3/NFT/DAO/Games category, which once dominated deal count, has slipped to fourth place in capital allocation.

This is VCs are finally prioritizing revenue-generating businesses over narrative-driven speculation.

The infrastructure that actually powers cryptocurrency transactions got funded.

Applications that people actually use got funded.

Protocols that generate real fees got funded.

And everything else will be increasingly starved of capital.

Artificial intelligence has also become a major competitor to venture capital.

Why bet on crypto games when you can bet on AI applications with a clearer revenue path? The opportunity cost of crypto-native applications has shifted significantly against projects that cannot demonstrate immediate utility.

Let’s dig into the data for the most sobering statistic: Crypto’s graduation rate from Seed to Series A is 17%.

That means five out of every six companies that raise a Seed round will never raise a meaningful follow-on round.

Compare that to the traditional tech industry where around 25-30% of Seed companies reach Series A, and you start to understand the severity of the problem.

Crypto’s success metrics have always been fundamentally flawed.

Why? Because for years, the crypto playbook was simple: raise venture money, build something that looks innovative, launch a token, and let retail investors provide exit liquidity. VCs didn’t need companies to actually graduate through funding rounds because the public markets would bail them out.

That safety net is gone. Most tokens issued in 2024 are trading at a fraction of their initial valuations. EigenLayer’s EIGEN, which launched at a fully diluted valuation of $6.5 billion, is now down 80%. There are only a handful of projects with more than $1 million in monthly revenue.

Whenthe road to token listings reaches its end, the true graduation rate begins to emerge. And the results are not optimistic. What is the result? VCs are now asking the same questions that traditional investors have been asking for decades: "How do you make money?" and "When will you make a profit?" This is obviously a revolutionary concept in the cryptocurrency space.

While the number of deals has dropped significantly, there have been interesting changes in deal sizes. The median seed round size has increased significantly since 2022, even though fewer companies are raising money overall.

This shows that an industry is consolidating around fewer and bigger bets. in the core circle, you may not get funding. If you don't get financing from top funds, your chances of getting subsequent financing will drop significantly.

This centralization isn’t limited to funding.

Data shows that 44% of companies in A16z’s portfolio have A16z participation in subsequent rounds.

For Blockchain Capital, the figure is 25%. The best funds are not only picking winners, they’re also actively ensuring their portfolio companies continue to get funded.

We’ve all witnessed the shift from “revolutionary DeFi protocols” to “enterprise blockchain solutions.”

Honestly? I’m conflicted.

Part of me misses the chaos. The wild swings. Anonymous teams with Discord nicknames raising millions for ideas that sound like fever dreams.

There was a purity in that craziness. It’s just that builders and believers are betting on a future that traditional finance can’t even imagine.

But another part of me — the part that has seen too many promising projects fail due to insufficient fundamentals — knows that this correction is inevitable.

For years, crypto VC has been operating in a fundamentally wrong way. Startups can raise money based on a white paper alone, launch tokens to retail investors for liquidity, and then call it success regardless of whether they have built something that users actually want.

The result? An ecosystem optimized for hype cycles rather than value creation.

Now, the industry is experiencing a long overdue shift from speculation to substance.

The market is finally starting to apply the performance standards that should have been there from the beginning. When only 17% of seed companies make it to Series A — it means market efficiency has finally caught up with an industry that was once artificially propped up by over-narratives.

All of this presents both challenges and opportunities. For founders used to raising money based on token potential rather than business fundamentals, the new reality is harsh. You need users, revenue, and a clear path to profitability.

But the environment has never been better for companies building real businesses that solve real problems. There is less competition for funding, investors are more focused, and the metrics for success are clearer.

The “tourist money” has left, leaving behind the deep pockets needed for real startups. The institutional investors that remain are not looking for the next “memecoin” or speculative infrastructure investments.

The founders and investors who survive this transition will build the infrastructure for the next chapter of crypto. Unlike the last cycle, this one will be built on business fundamentals, not token mechanics.

The gold rush is over. Mining operations have just begun.

Despite what I said about missing that chaos? It's exactly what cryptocurrencies need.

《华尔街日报》近日报道称,美国检察官正在调查 Tether 是否违反制裁和反洗钱法规,USDT 或被部分非法组织利用。Tether CEO 表示,公司致力于遵守国际制裁,不会与监管部门对抗。

AlexArthur Hayes 近日在采访中表示,他对 Solana 的未来潜力持积极态度,认为其表现或将超过比特币。同时,他指出美国大选的具体结果并非市场核心,真正影响加密市场的是即将公布的联准会利率决策。

Miyuki

Miyuki美国总统大选将于当地时间11月5日正式开启,本文分析了可能出现的四大选举情境,评估其中最有利于投资市场的情境以及可能导致市场震荡的风险。

Weiliang

WeiliangCraig Wright envisions transforming Bitcoin into a practical tool for financial inclusion through his proposed TerraNode, which aims to enhance Bitcoin's scalability and accessibility for users worldwide. He believes this system will eliminate high fees and barriers, empowering individuals excluded from traditional banking to engage in global trade without restrictions.

Anais

Anais稳定币发行公司Paxos在昨日(1日)发布公告,正式推出新型美元稳定币USDG(Global Dollar),该币种符合新加坡金融管理局(MAS)即将发布的稳定币监管框架的要求。

AlexTech giants Meta and Google face potential defamation risks as they integrate AI-generated user comments and reviews into their platforms, which could expose them to legal action if defamatory content is included. Recent legal rulings suggest that these companies could be held liable for such content, complicating the landscape of defamation law as technology continues to evolve.

Weatherly

Weatherly瑞士联合银行(UBS)推出了其首个基于以太坊区块链的代币化基金,显示出传统金融巨头对区块链技术的关注加深。加密分析人士认为,这将进一步推动以太坊(ETH)在传统金融生态中的地位,并可能带动ETH价格上涨。

MiyukiSingapore’s MAS is pushing forward with an ambitious asset tokenization plan, creating frameworks and commercial networks to integrate blockchain into traditional finance. With a test network for digital Singapore dollar transactions and global partnerships, Singapore aims to lead the tokenization market by 2030.

AnaisTaiwan is introducing new crypto regulations set to take effect in January 2025, focusing on compliance registration, stricter asset listing rules, and enhanced scrutiny for virtual asset service providers. The regulations aim to protect consumer interests by improving asset custody practices and establishing clear guidelines while emphasizing accountability and transparency in the crypto sector.

Weatherly新加坡主权基金淡马锡控股(Temasek Holdings)支持的区块链创投公司Superscrypt正筹备第二支创投基金,计划融资逾1亿美元,淡马锡将成为该基金的主要投资者和合作伙伴。

Weiliang