Larry Fink's Vision of Finance: Bitcoin, Ethereum, and the Future of Tokenization

Explore Larry Fink's, BlackRock CEO, insights on Bitcoin, Ethereum, and the transformative potential of ETFs and tokenization in shaping the future of finance.

Miyuki

Miyuki

Author: @Web3_Mario

Abstract: As Trump's policies are being fulfilled one by one, the combination of tariffs to attract manufacturing back to the country, the active detonation of the stock market bubble to force the Federal Reserve to cut interest rates and release water, and the deregulation policy to promote financial innovation and accelerate industrial development is actually changing the market. Among them, the RWA track under the favorable deregulation policy is also increasingly attracting the attention of the crypto industry. This article mainly introduces the opportunities and challenges of tokenized stocks.

In fact, tokenized stocks are not a new concept. Since 2017, attempts to STO have begun. The so-called STO (Security Token Offering) is a financing method in the field of cryptocurrency. Its essence is to digitize and chain the rights and interests of traditional financial securities and realize the tokenization of assets through blockchain technology. It combines the compliance of traditional securities with the efficiency of blockchain technology. As an important category of securities, tokenized stocks are the most concerned application scenario in the field of STO.

Before the emergence of STO, the mainstream financing method in the blockchain field was ICO (Initial Coin Offering). The rapid rise of ICO mainly relies on the convenience of Ethereum smart contracts, but the tokens issued by most projects do not represent real asset rights and interests, and lack supervision, resulting in frequent fraud and running away.

In 2017, the US SEC (Securities and Exchange Commission) issued a statement on the DAO incident, pointing out that some tokens may be securities and should be regulated by the Securities Act of 1933. This is the starting point for the formal germination of the STO concept. In 2018, STO became popular as a "compliant ICO" concept and began to attract attention from the industry. However, due to the lack of unified standards, poor liquidity in the secondary market, and high compliance costs, the market has developed slowly.

With the advent of DeFi Summer in 2020, some projects have begun to try to create derivatives linked to stock prices through smart contracts through decentralized solutions, so that on-chain investors can directly invest in the traditional stock market without the need for complex KYC processes. This paradigm is often referred to as the synthetic asset model. It does not directly hold U.S. stocks, and transactions do not require trust in centralized institutions, which can bypass expensive regulatory and legal costs. Representative projects include Synthetix and Mirror Protocol of the Terra ecosystem.

In these projects, market makers can mint synthetic U.S. stocks on the chain and provide market liquidity by providing excess cryptocurrency collateral, while traders can directly trade these targets through the secondary market in DEX to gain price exposure to anchored stocks. I still remember that the most popular stock in the U.S. stock market at that time was Tesla, not Nvidia in the previous cycle. Therefore, most project slogans have the selling point of trading TSLA directly on the chain.

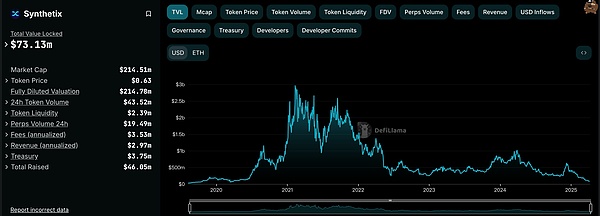

However, from the perspective of the final market development, the trading volume of synthetic US stocks on the chain has been unsatisfactory. Taking sTSLA on Synthetix as an example, including the casting and redemption in the primary market, the total cumulative on-chain transactions are only 798 times. Afterwards, most projects announced that they would remove synthetic assets of US stocks due to regulatory considerations and turn to other business scenarios. However, the fundamental reason is probably that they could not find PMF and could not establish a sustainable business model. The premise of the establishment of the business logic of synthetic assets is that there is a large demand for on-chain transactions, which attracts market makers to mint assets in the primary market and earn fees in the secondary market. If there is no such demand, market makers will not only fail to earn income through synthetic assets, but also have to bear the risk exposure of shorting anchored US stocks brought by synthetic assets, so liquidity will further shrink.

In addition to the synthetic asset model, some well-known CEXs are also trying to bring the ability to trade US stocks to Crypto traders through a centralized custody model. In this model, a third-party financial institution or exchange custody the actual stocks and directly create tradable targets in CEX. The more typical ones are FTX and Binance. FTX launched its tokenized stock trading service on October 29, 2020, in partnership with German financial company CM-Equity AG and Swiss Digital Assets AG, allowing users in non-US and restricted regions to trade tokens linked to stocks of US listed companies, such as Facebook, Netflix, Tesla, Amazon, etc. In April 2021, Binance also began to offer tokenized stock trading services, with Tesla (TSLA) being the first stock to go online.

However, the regulatory environment at the time was not particularly friendly, and the core initiator was CEX, which meant that it was in direct competition with traditional stock trading platforms, such as Nasdaq, and naturally came under considerable pressure. FTX's tokenized stock trading volume reached an all-time high in the fourth quarter of 2021. The trading volume in October 2021 was $94 million, but its tokenized stock trading service was discontinued after its bankruptcy in November 2022. Binance announced the suspension of tokenized stock trading services in July 2021, just three months after launching the business due to regulatory pressure.

Since then, as the market entered the bear market phase, the development of this track has also stagnated for a time. Until Trump's election, his deregulated financial policy brought about a change in the regulatory environment and rekindled the market's attention to tokenized stocks, but at this time it has a new name, RWA. This paradigm emphasizes the introduction of qualified issuers to issue tokens on the chain that are 1:1 secured by real-world assets through compliant architectural design, and the creation, trading, redemption, and management of secured assets are strictly implemented in accordance with regulatory requirements.

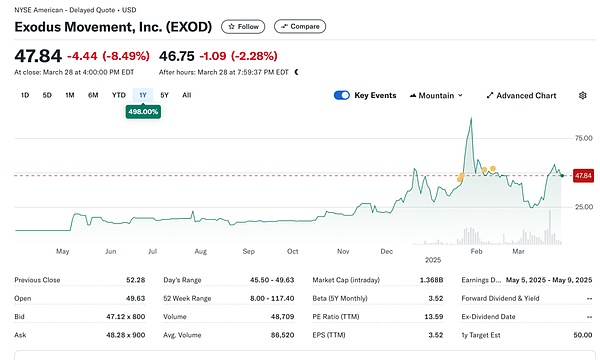

Next, let's introduce the current market status of stock RWA. In general, the market is still in its early stages and is still dominated by US stocks. According to data from RWA.xyz, the total issuance volume of the current stock RWA market has reached $445.40M, but it is worth noting that $429.84M of the issuance volume is attributed to a target, EXOD, which is an on-chain stock issued by Exodus Movement, Inc., a software company focused on developing self-hosted cryptocurrency wallets. The company was founded in 2015 and is headquartered in Nebraska, USA. The company's shares are listed on the New York Stock Exchange (NYSE America), and users are allowed to migrate their common Class A shares to the Algorand blockchain for management. Users can directly view the price of this part of the on-chain assets in the Exodus Wallet. The company's total market value is currently $1.5B.

The company has also become the only company in the United States to tokenize its common stock on the blockchain. But it is worth noting that the on-chain EXOD is only the on-chain digital identification of its stock, which does not contain voting, governance, economic or other rights. At the same time, the token cannot be directly traded and circulated on the chain.

This event has a certain symbolic significance, marking a clear change in the SEC's attitude towards on-chain stock assets. In fact, Exodus's attempt to issue on-chain stocks has not been smooth sailing. In May 2024, Exodus first submitted an application for common stock tokenization, but because the SEC's regulatory policy did not change at that time, the on-chain plan was initially rejected. But then in December 2024, after continuous improvement of technical solutions, compliance measures and information disclosure, Exodus finally obtained SEC approval and successfully completed the on-chain tokenization of common stock. This event also made the company's stock popular in the market, and the price reached an all-time high.

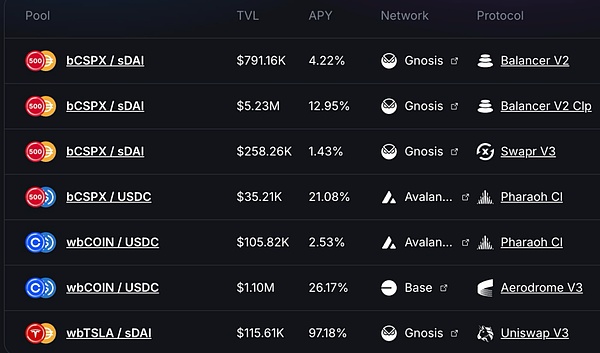

In addition, the remaining market share of about $16M is mainly attributed to a project called Backed Finance. This is a Swiss company that operates through a compliance framework, allowing users who meet KYC requirements to pay USDC to mint on-chain stock tokens through its official primary market. After receiving the crypto assets, Backed exchanges them for US dollars and purchases COIN stocks in the secondary market (there may be some delays in the middle due to the opening hours of the stock market). After the purchase is successful, the stocks are managed by a Swiss custodian bank, and then the 1:1 mint bSTOCK token is sent to the user. The redemption process is the opposite. The security of the reserve assets is guaranteed by an audit company called Network Firm, which regularly issues reserve certificates. On-chain investors can directly purchase such on-chain stock assets through DEXs such as Balancer. In addition, Backed does not provide stock token holders with ownership of the underlying assets or any other additional rights, including voting rights. And only users who have passed KYC can redeem USDC through the primary market.

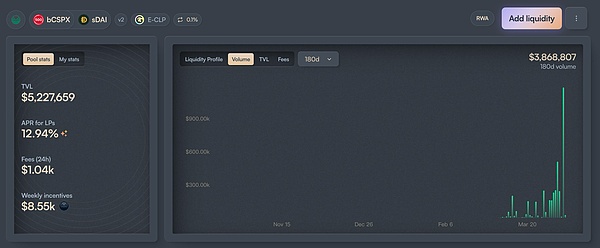

In terms of issuance, Backed's adoption is mainly concentrated on two assets, CSPX and COIN, of which the former has an issuance of about $10M and the latter is about $3M. In terms of on-chain liquidity, it is mainly concentrated on the Gnosis and Base chains, of which bCSPX has a liquidity of about $6M and wbCOIN has a liquidity of about $1M. In terms of transaction volume, it is not very high. Taking the largest liquidity pool of bCSPX as an example, since its deployment on February 21, 2025, the cumulative transaction volume is about $3.8M and the cumulative number of transactions is about 400 times.

Another trend worth paying attention to is the progress of Ondo Finance. As Ondo announced its overall strategy for Ondo chain and Ondo Global Markets on February 6, 2025, tokenized stocks are the core trading targets in its Ondo Global Markets. Perhaps Ondo, which has broader TradFi resources and better technical background, can accelerate the development of this track, but it remains to be seen.

Next, let's explore the opportunities and challenges of stock RWA. Generally speaking, the market believes that stock RWA has the following three advantages:

7-24 hour trading platform: Due to the technical characteristics of blockchain, it has the characteristics of 24-hour operation. This allows the trading of tokenized stocks to get rid of the trading hours of traditional exchanges and fully tap the potential trading demand. Take Nasdaq as an example. Although it has achieved the ability to provide 24-hour trading services by extending pre-market and after-market trading, the regular trading hours are limited to mid-week. If the trading platform is directly developed through blockchain, 24-hour trading will be achieved at a lower cost.

Low-cost access to US assets for non-US users: With the large-scale adoption of payment stablecoins, non-US users can directly use stablecoins to trade US assets without having to bear the handling fees and time costs brought by cross-border and cross-bank funds. Assuming that a Chinese investor invests in US stocks through Tiger Brokers, without considering the exchange fee, the cross-border remittance fee is about 0.1%. In addition, the settlement of cross-border remittances usually takes 1-3 working days. If transactions are conducted through on-chain channels, these two costs can be avoided.

The potential for financial innovation brought by composability: With its programmable characteristics, tokenized stocks will embrace the DeFi ecosystem, giving it stronger on-chain financial innovation potential. For example, scenarios such as on-chain lending.

However, the author believes that tokenized stocks are still facing two uncertainties:

The speed of regulatory policy advancement: Based on the cases of EXOD and Backed, we can know that the current regulatory policy cannot solve the problem of "same rights for stocks and coins" well, that is, the purchase of tokenized stocks and physical stocks has the same rights and interests at the legal level, such as governance rights. This limits many trading scenarios, such as corporate mergers and acquisitions through the secondary market. And the compliance use scenarios of tokenized stocks are still unclear, which has also hindered the pace of financial innovation to a certain extent. Therefore, its progress is very dependent on the speed of regulatory policy advancement. Considering that the core policy goal of the Trump administration is still in the stage of manufacturing repatriation, the timetable may continue to move back.

The development of stablecoin adoption: From the past development, the core target users of tokenized stocks are most likely not crypto-native users, but traditional, non-US US stock investors. For this group of people, whether the adoption of stablecoins is increasing is also a question worthy of attention, which will be closely related to the stablecoin policies of other countries. For example, for Chinese investors, compared with regular official channels for currency exchange, obtaining stablecoins through the OTC market requires a premium of about 0.3% to 1%, which is also much higher than the cost of investing in US stocks through traditional channels.

Therefore, in summary, in the short term, I believe that stock RWA has the following two market opportunities:

For listed companies, they can refer to the EXOD case and issue on-chain stock tokens. Although there are not many actual use scenarios in the short term, at least the potential financial innovation capabilities can make investors willing to give the company a higher valuation. For example, for some companies that can provide on-chain asset management services, this method can be used to transform investors into product users, and transform the stocks held by investors into the company's AUM, thereby enhancing the company's business growth potential.

For tokenized high-dividend US stocks, some income-based DeFi protocols will become potential users. With the reversal of market sentiment, the yields of most on-chain native real-income scenarios will drop significantly, and income-based DeFi protocols such as Ethena need to constantly look for other real-income scenarios to increase overall yields and enhance market competitiveness. For specific reference, please refer to the example of Ethena configuring BUIDL. High-dividend stocks usually belong to mature industries, with stable corporate profit models, sufficient cash flow, and the ability to continuously distribute profits to shareholders. Moreover, most of them have the characteristics of low volatility, strong ability to resist economic cycles, and relatively controllable investment risks. Therefore, if some high-dividend blue-chip stocks can be launched, they may be adopted by income-based DeFi protocols.

Explore Larry Fink's, BlackRock CEO, insights on Bitcoin, Ethereum, and the transformative potential of ETFs and tokenization in shaping the future of finance.

MiyukiExplore the UN's latest report in this comprehensive article, revealing how USDT is central to a clandestine banking system across Southeast Asia, raising significant concerns about digital currency misuse in money laundering and organized crime.

Brian

BrianExplore the intricate legal battle between Binance and the SEC in 'Binance Strikes Back: A Detailed Look at the Counter to SEC’s Terra Lawsuit Claims.' Delve into the complexities of cryptocurrency regulation, the application of the Howey Test in digital assets, and the potential implications for the future of digital currencies. This comprehensive article provides expert insights and a balanced perspective on this pivotal legal dispute.

Weiliang

WeiliangExplore the intricate legal battle between Coinbase and the SEC scheduled for a pivotal court decision on January 17, 2024. Understand the implications for cryptocurrency regulation and the future of digital assets.

MiyukiKakao Pay has been a prominent mobile payment and digital wallet service player in South Korea's financial landscape since its establishment in 2014.

Alex

AlexExplore how OpenSea is revolutionizing the NFT marketplace by onboarding millions into the Web3 space. This insightful article delves into OpenSea's strategies, challenges, and potential impacts on the cryptocurrency community and the digital economy.

BrianTUSD dipped below its peg around Jan. 15, at 11:00 am UTC, reaching as low as $0.984 by 11:15 pm.

AlexThe platform will service 420 DApps and services, 45 governance partners, and over 450 Web3 resources.

Davin

DavinExplore the dramatic story of a $9M Dogwifhat trade on Solana, its 60% loss due to slippage, and key lessons for cryptocurrency traders. Understand the risks and strategies in the volatile world of crypto trading.

WeiliangOn April 15-16, the international forum Blockchain Life 2024 will be at the main event of the year in Dubai.

Joy

Joy