Key Takeaways: Demand from major absorption channels such as ETFs and DAT has weakened recently, while the deleveraging events of October and the macroeconomic backdrop of declining risk appetite continue to put pressure on the crypto asset market. Leverage in the futures and DeFi lending markets has been reset, resulting in lighter and cleaner positions, thus reducing systemic risk. Spot liquidity has not yet recovered; both mainstream assets and altcoins remain weak, making the market more vulnerable and susceptible to unexpected price fluctuations.

Introduction

“Uptober” started strongly, driven by Bitcoin hitting a new all-time high. But the optimism was quickly interrupted by the flash crash in October. Since then, BTC has fallen by about $40,000 (over 33%), altcoins have been hit even harder, bringing the overall market capitalization close to $3 trillion. Despite positive fundamentals this year, price performance has clearly diverged from market sentiment.

Digital assets seem to be at the intersection of multiple external and internal forces. On the macro level, uncertainty about a December rate cut and the recent weakness in tech stocks have exacerbated the decline in risk appetite.

Within the crypto market, core absorption channels such as ETFs and Digital Asset Vaults (DATs) are experiencing outflows and increased cost pressures. Meanwhile, the market-wide liquidation that occurred on October 10th triggered one of the most severe deleveraging events in recent years, and its aftershocks continue as market liquidity remains shallow. This report will dissect the drivers behind the recent weakness in the crypto asset market. We will delve into ETF flows, perpetual futures and DeFi leverage, and order book liquidity to explore how these changes reflect the current market conditions. The macroeconomic environment is shifting towards a decline in risk appetite. The performance divergence between Bitcoin and major asset classes is widening. Gold has risen more than 50% year-to-date, driven by record central bank demand and ongoing trade tensions. Meanwhile, tech stocks (NASDAQ) lost momentum in the fourth quarter as the market reassessed the probability of a Fed rate cut and the sustainability of AI-driven valuations. As our previous research has shown, the relationship between BTC and "risk assets" tech stocks and "safe-haven assets" gold fluctuates cyclically with the macro environment. This means it is particularly sensitive to sudden events or market shocks, such as the flash crash in October and the recent decline in risk appetite. As the anchor for the entire crypto market, Bitcoin's pullbacks continue to ripple through other assets, although themes such as privacy occasionally show brief gains, but overall remain in sync with BTC.

ETFs and DAT: Weakening Absorption Demand

Part of the reason for Bitcoin's recent weakness is that the absorption channels that have been supporting it for most of 2024–2025 have begun to weaken. Since mid-October, ETFs have seen net outflows for several consecutive weeks, totaling $4.9 billion. This is the largest round of redemptions since April 2025, when Bitcoin fell to around $75,000 due to tariff expectations. Despite the significant short-term outflows, on-chain holdings are still on an upward trend, with the BlackRock IBIT ETF alone holding 780,000 BTC, accounting for about 60% of the total supply of spot Bitcoin ETFs.

ETFs and DAT: Weakening Absorption Demand

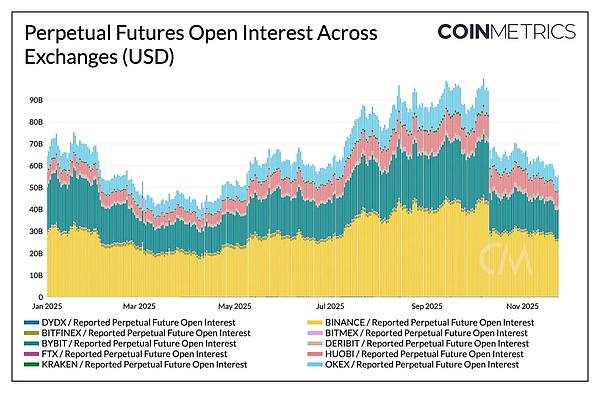

If funds return to a sustained net inflow, it will signify that this channel is stabilizing. Historically, ETF demand has been a key absorber of supply when risk appetite improves. Digital Asset Vaults (DATs) are also facing pressure. As markets decline, the market capitalization of their equity and crypto holdings is compressed, putting pressure on the net asset value premium that underpins their exponential growth mechanism. This will limit their ability to raise new capital through stock issuance or debt issuance, thus limiting their potential to increase their “per-crypto asset” allocation. Smaller or newer DATs are particularly sensitive to this change and will be more cautious when cost bases and equity pricing become unfavorable. Strategy—currently the largest holder of DAT—holds 649,870 BTC (approximately 3.2% of the total supply) at an average cost of $74,333. As shown in the chart below, Strategy's accumulation accelerated significantly when BTC rose and its stock price performed strongly, but has slowed noticeably recently, though it hasn't become a force for active selling. Even so, Strategy remains in a profit position with a cost basis below the current price. If BTC falls further, or if it faces the risk of being removed from the index, Strategy may face pressure; however, if the market reverses and its balance sheet and valuation improve, it is expected to resume a stronger accumulation pace. The on-chain profitability metrics also reflect this situation. Short-term holders' SOPR (<155 days) has fallen into a loss range of ~23%, which usually indicates a "capitulation" sell-off by the most sensitive holding group. Long-term holders are still in profit on average, but SOPR also shows a mild selling tendency. If STH SOPR returns above 1.0, while LTH selling pressure eases, it means the market may have stabilized again. Crypto Market Deleveraging: Perpetual Futures, DeFi Lending, and Liquidity The liquidation wave on October 10th triggered a multi-layered deleveraging cycle spanning futures, DeFi, and stablecoin leverage, the effects of which have not yet fully dissipated. The Perpetual Futures Leverage Cleanup Within just a few hours, perpetual futures experienced the largest forced deleveraging in history, wiping out more than 30% of the open interest accumulated over several months. Altcoins and platforms with a high retail market share (such as Hyperliquid, Binance, and Bybit) experienced the deepest declines, consistent with the aggressive leverage accumulated in these sectors previously. As shown in the chart below, current open interest remains significantly lower than the pre-flash crash high of over $90 billion, and subsequently declined slightly further. This indicates that leverage within the system has been significantly cleared, and the market has entered a stabilization and repricing phase. Funding rates have also decreased in tandem, reflecting a reset in bullish risk appetite. BTC funding rates have recently hovered in neutral or slightly negative territory, consistent with the market's lack of clear directional confidence.

DeFi Deleveraging

The DeFi lending market has also undergone a gradual deleveraging process. Active lending on Aave V3 has been declining steadily since its peak at the end of September as borrowers reduced leverage and repaid debts. The contraction in stablecoin lending was most pronounced, with the de-pegging of USDe causing a 65% drop in USDe lending volume and further triggering a liquidation chain of synthetic dollar leverage.

DeFi Deleveraging

The DeFi lending market has also undergone a gradual deleveraging process. Active lending on Aave V3 has been declining steadily since its peak at the end of September as borrowers reduced leverage and repaid debts. Stablecoin lending contracted the most, with USDe de-pegging causing a 65% drop in USDe lending volume and further triggering a liquidation chain of synthetic dollar leverage.

Weatherly

Weatherly