Did Regulation Indirectly Create FRAX, Nifty Gateway, and TornadoCash?

If you were to sit down and really think, it's almost as if regulatory scrutiny and the tribulations that they have faced has shaped the industry in some sense.

Snake

Snake

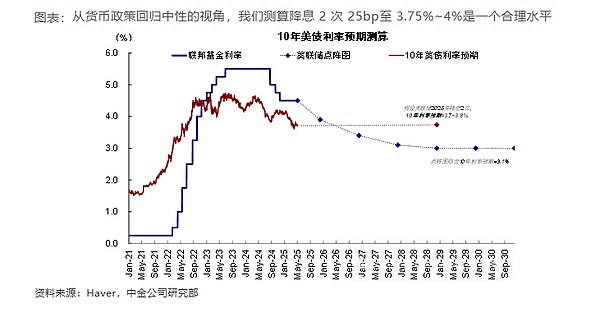

Under the baseline scenario, CICC expects the Federal Reserve to cut interest rates one to two times this year, lowering the policy rate to a range of 3.75% to 4%.

CICC Research Department Macroeconomic Analyst Xiao Jiewen and others believe that

At its most recent meeting, the Federal Reserve decided to remain on hold, with Chairman Powell and most officials leaning toward maintaining a tightening stance. They believe that inflation risks posed by tariffs have not been fully resolved, and the labor market remains solid, making the conditions for a rate cut unnecessary. Powell acknowledged that current policy is "moderately restrictive," but argued that this is not sufficient grounds for a rate cut, and that the Fed needs to "remain patient." A more critical factor is the Fed's independence. Facing political pressure for a rate cut, Powell made it clear that the Fed will not adjust its interest rate path. Its policy goals are full employment and stable inflation, not helping governments reduce debt costs. The report emphasizes that the market may be underestimating the Fed's resolve to maintain its independence. The Federal Reserve held its July meeting steady, in line with market expectations. Two board members dissented from holding interest rates steady, but Powell and the majority of officials favored maintaining a tight policy stance. They argued that the inflationary risks posed by tariffs remain lingering, and the labor market remains solid, making a rate cut unnecessary. Powell also emphasized the Fed's independence, suggesting it would not succumb to political pressure. We believe that the inflationary effects of tariffs will become more pronounced in the coming months, making it difficult for the Fed to cut interest rates in September. If Trump continues to escalate tariffs, the timing of a rate cut could be delayed. As for Trump's pressure for a rate cut, we believe the market underestimates the Fed's resolve to maintain its independence.

The interest rate decision is jointly decided by 12 voting committee members. Even if Trump fires Powell, it will be difficult to change the direction of monetary policy.

If you were to sit down and really think, it's almost as if regulatory scrutiny and the tribulations that they have faced has shaped the industry in some sense.

SnakeMeta unveils research using MEG technology that advances real-time decoding of how our brains perceive and process images.

YouQuan

YouQuanGeorgia-based physician, Dr. James Wan, recently entered a guilty plea for masterminding a murder-for-hire plot utilising Bitcoin on the dark web.

Jasper

JasperThis decision marks a continuation of the status quo established after the company's significant sell-off of Bitcoin in Q2 2022, when it liquidated approximately 75% of its holdings for $936 million.

JasperThe prices of related tokens like MOON, BRICK, and DONUT have taken a hit.

Clement

ClementBoth companies have expressed their intent to leverage OpenAI's models in sectors where G42 boasts expertise and connections, such as energy, finance, healthcare, and public services.

Kikyo

KikyoNavigating California's cryptocurrency regulation and anticipating potential industry consequences.

Hui Xin

Hui XinAptos Resumes Network After 5-Hour Outage

Aaron

AaronChainalysis doubts reports on terrorists using cryptocurrency, with concerns about exaggerations following the recent Hamas attack in Israel.

JasperThe newly launched T wallet is a blockchain-based mobile app and provides access to CryptoQuant's on-chain analysis tools.

Alex

Alex