DeFi Revival: What is the Future of BTCFi?

As the U.S. regulation of virtual currencies becomes increasingly clear, DeFi has also become one of the main themes of this bull market.

JinseFinance

JinseFinance

Written by: Umbrella

On August 27th, the BTC ecosystem project BitLayer was listed on Binance Alpha. This once highly anticipated BTCFi star project, however, suffered a significant drop that marked the entire sector.

According to CMC data, BTR opened at 0.1511, plummeting to 0.077 within a few hours, a single-day drop of 48.6%. As of August 28th, the token remains down 44.3% from its all-time high, with a 24-hour trading volume of $60.3 million, resulting in a volume-to-market-cap ratio of 274%. This extreme speculative turnover exposes the embarrassing lack of long-term holders for the project. Even more thought-provoking is that, despite the on-chain TVL remaining at a relatively high $429 million, the precipitous drop in token price clearly reflects market skepticism about the BTCFi ecosystem's ability to capture value. BitLayer's opening plunge is far more than just a case of "peak coin listing"; it also epitomizes the entire BTCFi narrative's decline from frenzy. The Collective Decline of Mainstream Projects The BTC ecosystem has previously produced numerous phenomenally popular projects, but none of them conceal their inherent flaws and narrative inconsistencies. Merlin Chain: TVL of 3.8 Billion Now Only 50 Million As a former BTCFi leader, Merlin Chain's performance has been nothing short of breathtaking. Within 50 days of its launch, the project attracted $3.8 billion in BTC pledged, reaching a peak TVL of $530 million, briefly becoming the leading BTC Layer 2 project in terms of both TVL and user base. However, the reality is stark: according to DeFillama data, Merlin Chain's current TVL is only $50 million, a plunge of over 90% from its peak. The price of its Merl token is hovering around $0.115. Despite a 45.1% year-to-date increase, it remains 90% below its all-time high. Even more heartbreaking is its 24-hour on-chain inflow of only $1,946.

It took only half a year for Merlin Chain to go from being the undisputed leader in its field to being condemned by everyone like a rat crossing the street. To this day, people still occasionally mention Merlin, but it is almost entirely with sarcasm and complaints.

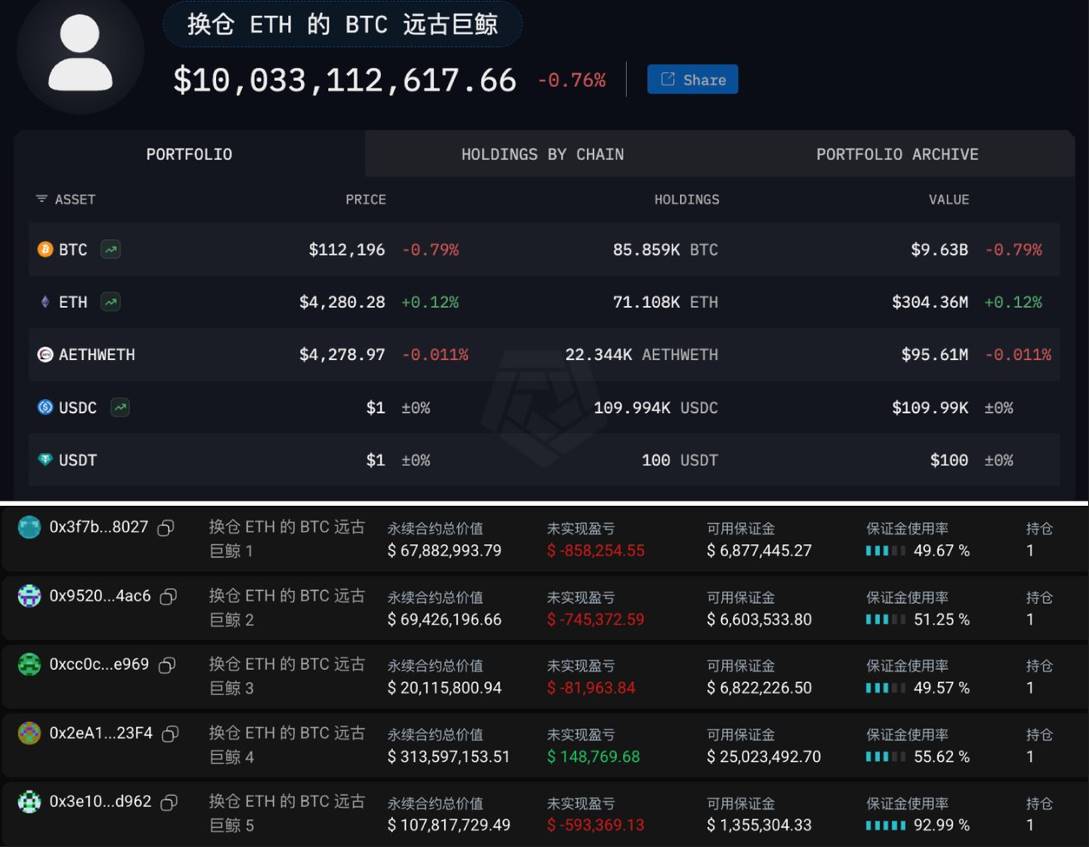

The Ordinals inscriptions and BRC-20 tokens that once ignited the BTC ecosystem are now no longer as popular as they used to be. Looking back at the winter of the crypto-inscription craze, every public blockchain launched its own inscription product, igniting a nationwide craze. Bitcoin, the origin of everything in the crypto world, gave rise to popular projects like Sats and Ordi. The slogan "Buy an Ordi today, drive an Audi tomorrow" still rings in our ears. Today, the phrase "Ordinals are dead" has evolved from a mockery into a self-deprecating meme within the crypto community, with even the official accounts of crypto-inscription projects using the meme to mock themselves. The BTC NFT market has fewer than 2,000 24-hour active users, accounting for 1.7% of total chain activity, far lower than the ETH or Solana ecosystems. The actual uses of inscriptions and NFTs remain a hotly debated topic in the market, but once-active users are leaving one after another. This loss of user confidence suggests that the importance of this narrative is gradually fading in people's minds as the crypto market accelerates. In addition to Merlin Chain, BTC inscriptions, and NFTs, other BTCFi projects have also gradually exposed their own shortcomings or flaws in their models. Babylon's current TVL has reached a record high of $6.3 billion, but its price has plummeted 77% from that peak, exposing its shortcomings in its single staking model and its lack of innovative applications. Core, another popular project in the BTC ecosystem, currently has a TVL of only $386 million, down over 70% since the beginning of the year. The truth behind the data is even more grim: with the exception of Babylon, most BTCFi projects generate less than $50,000 in daily fee revenue, far below the millions of dollars earned by traditional DeFi projects. The unsustainability of this business model is being ruthlessly exposed by the market. Narrative Fatigue and Inherent Contradictions BTCFi's fundamental dilemma stems from the technical limitations of BTC itself. As "digital gold," BTC is designed without the programmability of smart contracts, forcing all BTCFi applications to rely on compromised solutions such as sidechains, Layer 2 (L2), or cross-chain bridges. According to DeFillama data, bridged assets currently account for 80%-100% of the TVL of mainstream BTCFi projects: Merlin Chain's bridged TVL accounts for as much as 80%, Core's 94%, and Bitlayer's near-100% reliance on BTC cross-chain. This extreme reliance on cross-chain infrastructure not only increases security risks but also violates BTC's core spirit of decentralization and autonomy. On social media, discussions about BTCFi have shifted from early excitement and exploration to a "prove-your-worth" phase of skepticism. A growing number of influencers (KOLs) are also labeling the BTC ecosystem as a doomed venture. The attitude of retail investors is self-evident. Their expectations for the BTC ecosystem are being repeatedly diluted by the fresh narratives of ETH and SOL. The recent surge in whales selling BTC in exchange for ETH has undoubtedly poured cold water on this smoldering market.

Image source: @Ai姨

On the other hand, the dire state of the BTC ecosystem also reveals the inherent contradictions in the economic models of most BTCFi projects.

To attract liquidity, project developers must offer high-yield incentives, but high returns often rely on token issuance, which dilutes long-term value.

BitLayer's extremely high turnover rate and Merlin Chain's user churn both demonstrate the unsustainability of this mine-and-dump model. BTC, Returning to a Spiritual Totem Looking back at the rise and fall of BTCFi, we may need to re-examine BTC's position in the crypto ecosystem. Unlike ETH, which was designed from the outset as a "world computer," BTC is more of a crypto totem, and the role of a totem lies in consolidating consensus and belief rather than expanding functionality. ETH is able to support the DeFi ecosystem because its architecture is optimized for programmability. BTC's value proposition, however, has never been about "what it can do" but rather "what it represents." Perhaps when we try to make BTC support complex financial applications, we've already betrayed its essence. Compared to BitLayer and Merlin, Babylon is relatively successful. Its success demonstrates that, as a pure BTC staking protocol, it doesn't attempt to change BTC, but rather leverages BTC's security to provide services to other chains. This "specialization" approach may be the right way for BTC to participate in DeFi.

The decline of BTCFi is not a failure of BTC, as evidenced by BTC's continuous breakthroughs to new highs this year. Rather, BTCFi is more like the market's rational correction to excessive financialization.

BTC remains the most important store of value in the crypto world, but it will never and should never become the next ETH.

Recognizing this point may be a sign of the industry's maturity.

As the U.S. regulation of virtual currencies becomes increasingly clear, DeFi has also become one of the main themes of this bull market.

JinseFinanceMany people only saw the continuous surge of $XRP, but they didn’t know that $FLR also followed the 3-fold increase. I can’t help but ask, what is the relationship between Ripple and Flare Network? After BTCFi, will XRPFi also become a new narrative?

JinseFinanceBitcoin’s role in DeFi (decentralized finance) is changing dramatically. From being a simple peer-to-peer transfer, the world’s first cryptocurrency is now gradually emerging as a powerful force in the DeFi field.

JinseFinanceBTCFi L2/L1 has three development pain points: lack of consensus on the UTXO architecture, fragmentation of views within the Bitcoin ecosystem, and lack of consensus on the definition of Bitcoin L2.

JinseFinance本文从比特币编程的可行性与演进路径入手,系统探讨了比特币在去中心化金融(BTCFi)领域的潜力与挑战。

JinseFinanceBabylon can provide secure, cross-chain-free, and custody-free native staking solutions for PoS chains including BTC layer2, and promote cross-chain interoperability. It is often compared to the Eigenlayer of the Ethereum ecosystem.

JinseFinanceHow does Babylon work? What is the difference between Babylon and Eigenlayer? What are the potential highlights of Babylon ecosystem? What are the weaknesses of Babylon?

JinseFinanceMost of the second layers of Bitcoin are pseudo-concepts. What we should really do is to broaden the application scenarios of BTC, especially BTCFi.

JinseFinanceCipher, co-founder of CKB and proposer of RGB++, talked about the unique significance of RGB++ Layer and UTXO model to BTCFi, and some questions and opinions about CKB and Bitcoin ecology.

JinseFinanceHow we got here, what to do on Bitcoin now, and what the future holds.

JinseFinance